> ## Documentation Index

> Fetch the complete documentation index at: https://docs.synctera.com/llms.txt

> Use this file to discover all available pages before exploring further.

# Card Transaction Lifecycles

> This document is to provide end to end maps of common card transaction lifecycles.

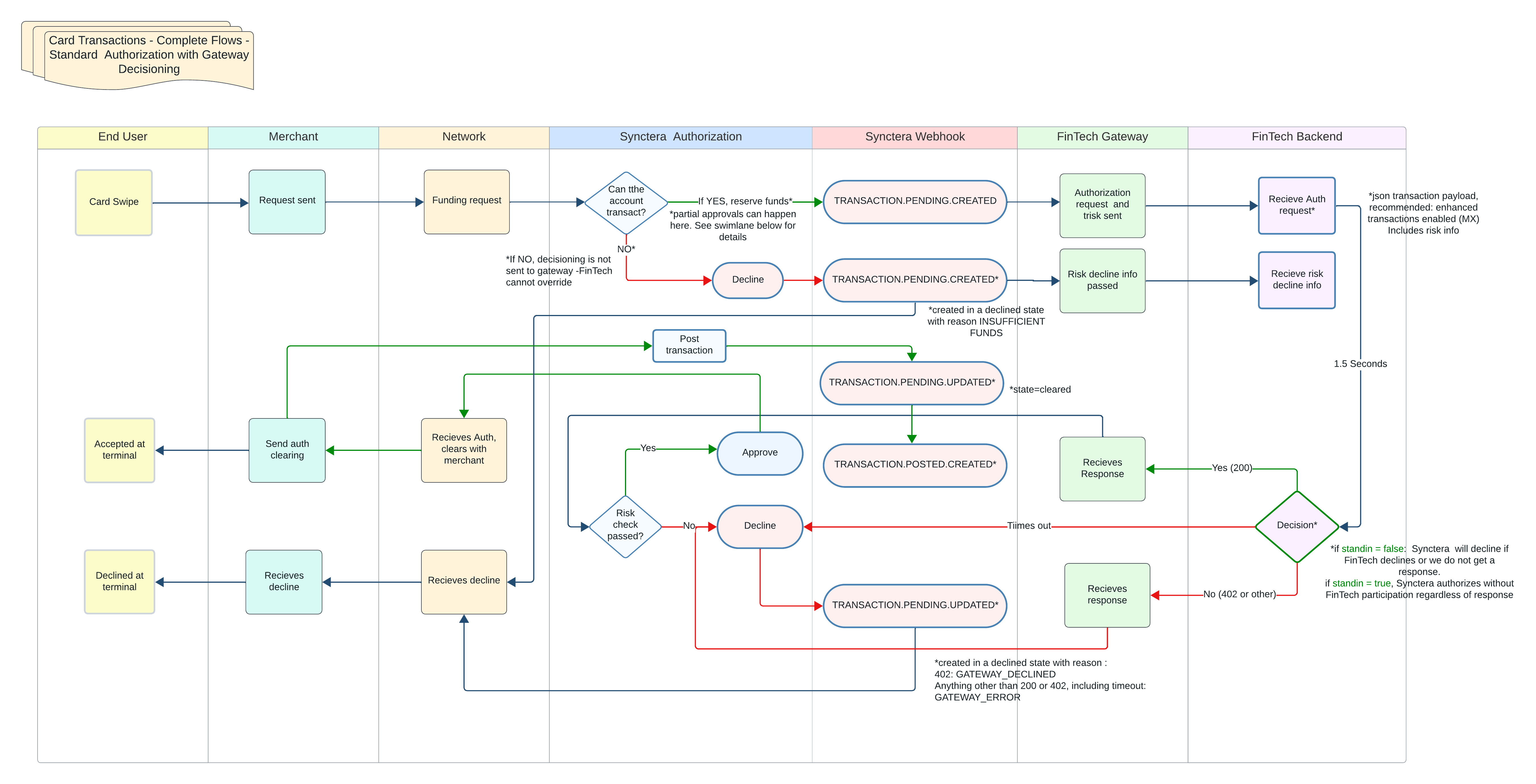

## Card Transaction Lifecycles

There are various flows that can happen regarding the lifecycle of a transaction, including standard authorization, AFDs (including Advice, Single Transaction, and Multiple Clearings). See maps below for holistic overviews of these lifecycles, and our full [Card Transactions Guide](/docs/card-transactions) for more details. To participate in auth decisioning, use our [/v0/cards/gateways](/v2/reference/creategateway) endpoint.

### Standard Authorization w/ Gateway

*Coming soon: Maps for AFDs!*

### **FAQs**

* No. Synctera is the issuer processor, not the merchant. Once a transaction is approved, Synctera no longer has any control over state changes. The customer would have to reach out to the merchant to inquire further.

* When we approve a transaction, we check things like card, customer, and account eligibility, and account balance. Once approved, we have no further control over what happens to a transaction beyond deciding if increase or decrease requests from the merchant are approved.

* If the transaction was approved before the freeze, the posting cannot be rejected. We can only update the ledger accordingly when the message tells us the transaction has cleared.

* When we approve a transaction, we check things like card, customer, and account eligibility, and account balance. Once approved, we have no further control over what happens to a transaction beyond deciding if increase or decrease requests from the merchant are approved.

* If the transaction was approved at a point when the account balance was sufficient, and then some other forced transaction occurred that drew the balance below the pending amount, the posting cannot be rejected.

* For certain merchant types that involve tips, the flow is that we authorize the purchase amount, and the customer leaves a tip after the authorization has been approved. This makes its way to us as a forced clearing for an amount greater than the authorization. The merchant captured these funds, and the network will take it from the bank. There is no way to stop this from happening even if it draws an account negative.

*Coming soon: Maps for AFDs!*

### **FAQs**

* No. Synctera is the issuer processor, not the merchant. Once a transaction is approved, Synctera no longer has any control over state changes. The customer would have to reach out to the merchant to inquire further.

* When we approve a transaction, we check things like card, customer, and account eligibility, and account balance. Once approved, we have no further control over what happens to a transaction beyond deciding if increase or decrease requests from the merchant are approved.

* If the transaction was approved before the freeze, the posting cannot be rejected. We can only update the ledger accordingly when the message tells us the transaction has cleared.

* When we approve a transaction, we check things like card, customer, and account eligibility, and account balance. Once approved, we have no further control over what happens to a transaction beyond deciding if increase or decrease requests from the merchant are approved.

* If the transaction was approved at a point when the account balance was sufficient, and then some other forced transaction occurred that drew the balance below the pending amount, the posting cannot be rejected.

* For certain merchant types that involve tips, the flow is that we authorize the purchase amount, and the customer leaves a tip after the authorization has been approved. This makes its way to us as a forced clearing for an amount greater than the authorization. The merchant captured these funds, and the network will take it from the bank. There is no way to stop this from happening even if it draws an account negative.