Synctera Instant Account Funding

Synctera offers Instant Account Funding as an alternative to other funding methods in your payment strategy. This is a convenient method that operates through existing card networks (Visa Direct and Mastercard MoneySend) to speed up funds delivery. This method offers 24/7/365 availability and allows customers to pull funds from their payment card to instantly fund their account.Other names for Instant Account FundingThroughout the payments industry, this payment method is also known as an “Account Funding Transaction” (AFT) or an “instant purchase”

Benefits

Adding Synctera Instant Account Funding to your payment stack enables you to:- Increase conversions: Make your financial product or FinTech app more attractive to potential customers by providing immediate access to funds

- Increase stickiness: Get customers using your product soon after signing up

- Increase customer satisfaction: Deliver real-time, convenient payment experiences to support growing customer demand.

Use cases

- Immediate (and subsequent) funding of a new account - provides faster access to secured funds with a cardholder name match or EMV 3DS

- Top-up of a stored value account

- Funding for payouts, e.g. daily pull from a business card to distribute employees’ wages after each shift

- Funding to support recurring purchases, such as subscriptions or utility bills

Considerations

Eligibility and supported scenarios

What we currently support:- Domestic transfers with Visa/Mastercard debit cards that are enabled for instant transfer services, which includes most debit cards

- Commercial and consumer debit cards

- Cross-border transfers

- Transfers with credit cards

Cost/pricing

- Because you act as a merchant, you pay interchange and network fees

- The interchange fee for unregulated debit is higher for than for regulated debit

- Interchange and network fees are billed monthly

- You can add a markup / convenience fee for your customers

- Contact Synctera for detailed pricing

Limits

Network limits:

| Consumer cards | |

|---|---|

| Per transaction | $2,500* |

| Daily limit per card | $10,000 |

| Business cards | |

| Per transaction | $2,500* |

| Daily limit per card | $10,000 |

Processor limits:

| Consumer cards | |

| Per transaction | $2,500* |

| Daily limit per card | $10,000 |

| Business cards | |

| Per transaction | $2,500* |

| Daily limit per card | $10,000 |

Other limitsPer-transaction and velocity limits may also be set by you and/or your sponsor bank

Risk management

With correct measures in place, instant account funding transactions are relatively secure. The following fraud prevention mechanism are utilized at different points in the instant transfer lifecycle to reduce fraud and chargebacks: During onboarding:- KYC/KYB on account holder

- Tokenization of card

- Address Verification Service (AVS) to verify cardholder address (address on card matches address on file)

- Cardholder name check (name on card matches name on file)

- Check that customer and account are in good standing

- Limit checks

- Check fraud rules

- [Coming soon] EVM 3DS (added layer of cardholder authentication):

- Note that this requires additional 3DS SDK integration

- OFAC check (if required for use case)

- Eligibility check

- Monitoring of account and transaction activity

- Anti-Money Laundering (AML) program

Chargebacks

- Synctera will notify you of any chargebacks that are opened by the cardholder through the issuer.

- When a chargeback is opened, the cardholder’s payment is immediately reversed and your settlement account is debited.

- As the merchant, you can dispute chargebacks by uploading relevant evidence within 10 calendar days of the exception date. Synctera will guide you through this process.

- The evidence is reviewed by the Issuer, who determines the outcome of the case.

- Chargeback fees are billed monthly.

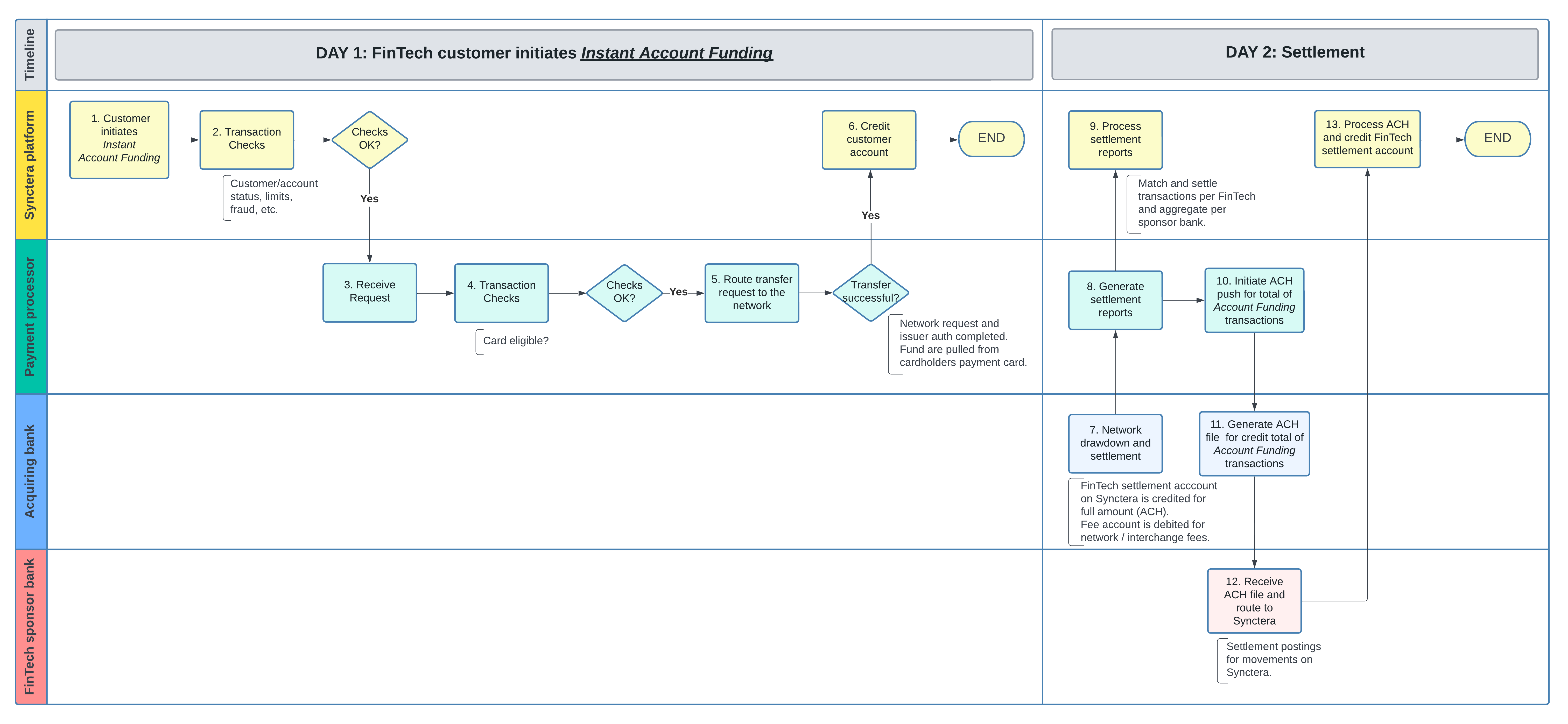

Flow of funds

Prerequisites:- FinTech customer has been onboarded on the Synctera platform and passed KYC/KYB

- FinTech customer has successfully added/linked their external card

Although the customer account is funded immediately, your sponsor bank does not receive the funds until settlement (day 2). Therefore, your sponsor bank will require additional reserves from you to cover the liquidity for your forecasted daily total of Instant Account Funding for one or more days (since settlement only occurs on business days).