Overview

The main responsibilities of the bank are explained in the following sections.Image review for custom cards

Some FinTechs support custom card programs, where users can upload images to include on the front of their physical cards. When these images are uploaded to Synctera, a Custom Card Review case is created for manual review. The bank can defer this review process to the Synctera Operations Team or manage it themselves. Information about the review process can be found [here].Fraud management

Synctera Fraud helps FinTechs to provide the proper oversight and controls to prevent fraud. Not only can card fraud have a signifiant impact on FinTech’s bottom line - it can also damage the bank’s reputation and regulatory standing. Information about the process can be found here. The card networks also have Fraud Reporting requirements that the issuing bank must comply with.Mastercard Fraud Reporting requirements

Content coming soon.Visa Fraud Reporting requirements

Content coming soon.Dispute management

Synctera will manage and process disputes that are raised by the cardholder through Synctera Cases and its vendor partner. The bank will have rights to review, approve and audit the dispute management process. Information about the process can be found [here].Network reporting requirements

In addition to Fraud Reporting requirements described above, the networks may require the Principal Member / issuing bank to submit reports on their debit card programs on regular intervals.Mastercard Reporting requirements

Mastercard mandates Principal Members of Mastercard to submit Quarterly Mastercard Reporting (QMR) to Mastercard. The QMR was described in the Bank Start Guide.Visa Reporting requirements

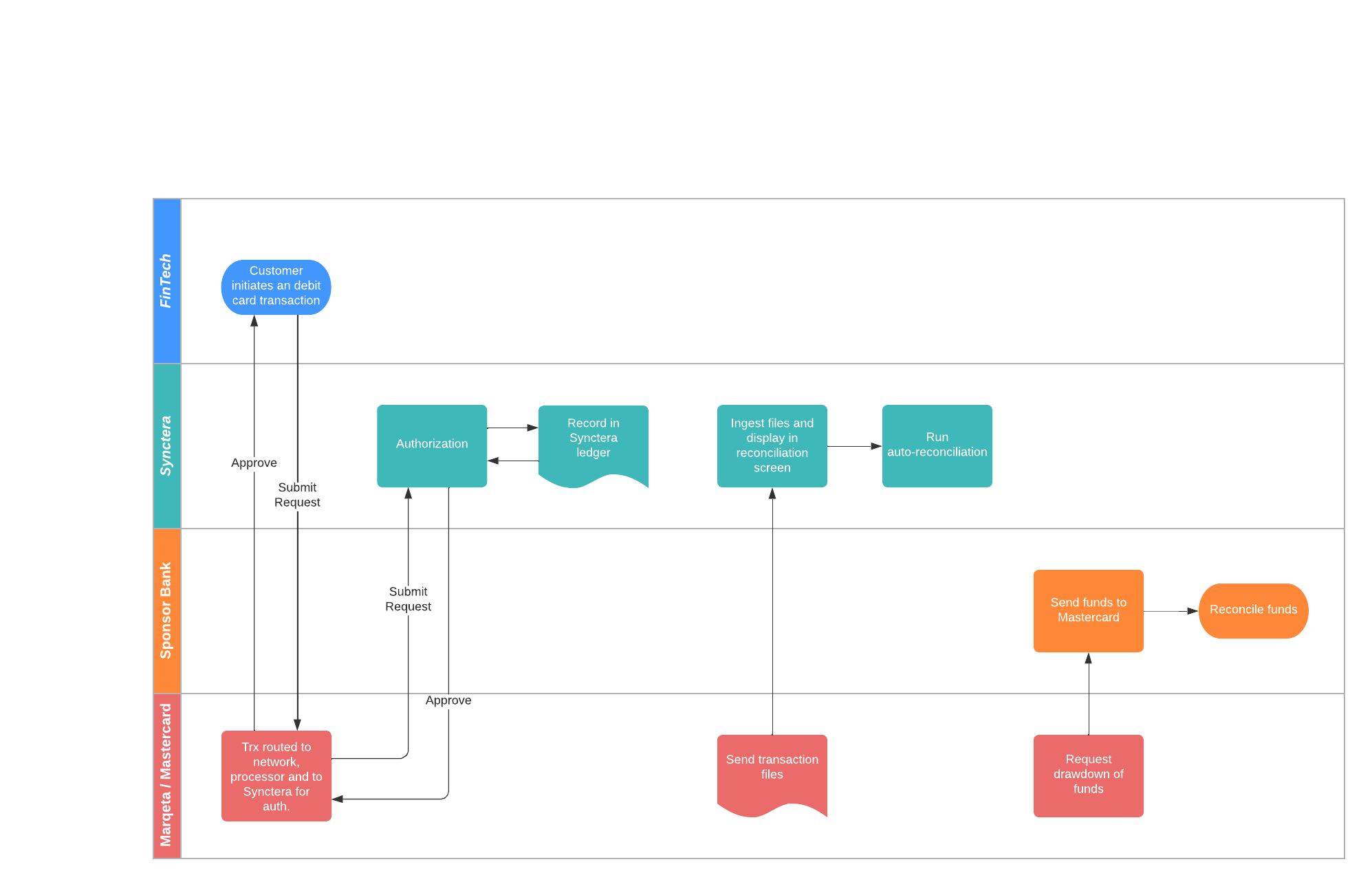

Content coming soon.Daily settlement and reconciliation

Information on Synctera Debit Card reconciliation and daily settlement can be found here.Roles & Responsibilities