Customer Support, Disputes, and Complaints

This includes fielding requests on how your app works, technical issues, and customer complaints.- Your customer support policy or guide should describe your general process and tools for responding to your customers.

- Your Sponsor Bank will be especially interested in how you interact with consumers (if applicable) as there are general guidelines and rules pertaining to consumer complaints and transaction disputes. This includes a responsibility of your Company to log customer complaints that you receive directly or through regulators such as the Federal Reserve or Consumer Financial Protection Bureau. Managing these complaints promptly and addressing any major themes that occur can protect you from reputation and legal risks.

- It also includes ensuring that you follow the response timelines and have the ability to provide provisional credits to consumers according to Regulation E, which addresses consumer disputes on electronic transactions such as debit card and ACH transactions. In addition, there are cases where fraudsters may file disputes and having trained experts manage the responses can help mitigate fraud losses or excessive issuance of provisional credit by the Company.

Reg E Disputes

Customers can dispute transactions for many reasons ranging from not recognizing the transaction to fraudulent transactions by an unauthorized user. The most common reasons for disputes are as follows:- Amount discrepancy

- Duplicate/Unauthorized transaction

- Victim of fraud, card theft, or identity theft

- Returned merchandise (generally not covered by Reg E)

- Product/Service not as described or not received (generally not covered by Reg E)

Reg E DisputesReg E outlines rules for electronic funds transfers between consumers and financial institutions. This covers transfers made through ATMs, point-of-sale transactions, and ACH systems.It was created by the U.S. Federal Reserve to enforce the Electronic Funds Transfers Act, which was passed in 1978 by the U.S. Congress to safeguard consumers participating in financial transactions like these.Reg E disputes have specific timelines and steps that must be followed. Only certain types of disputes are considered Reg E disputes and the regulation only covers consumer disputes.

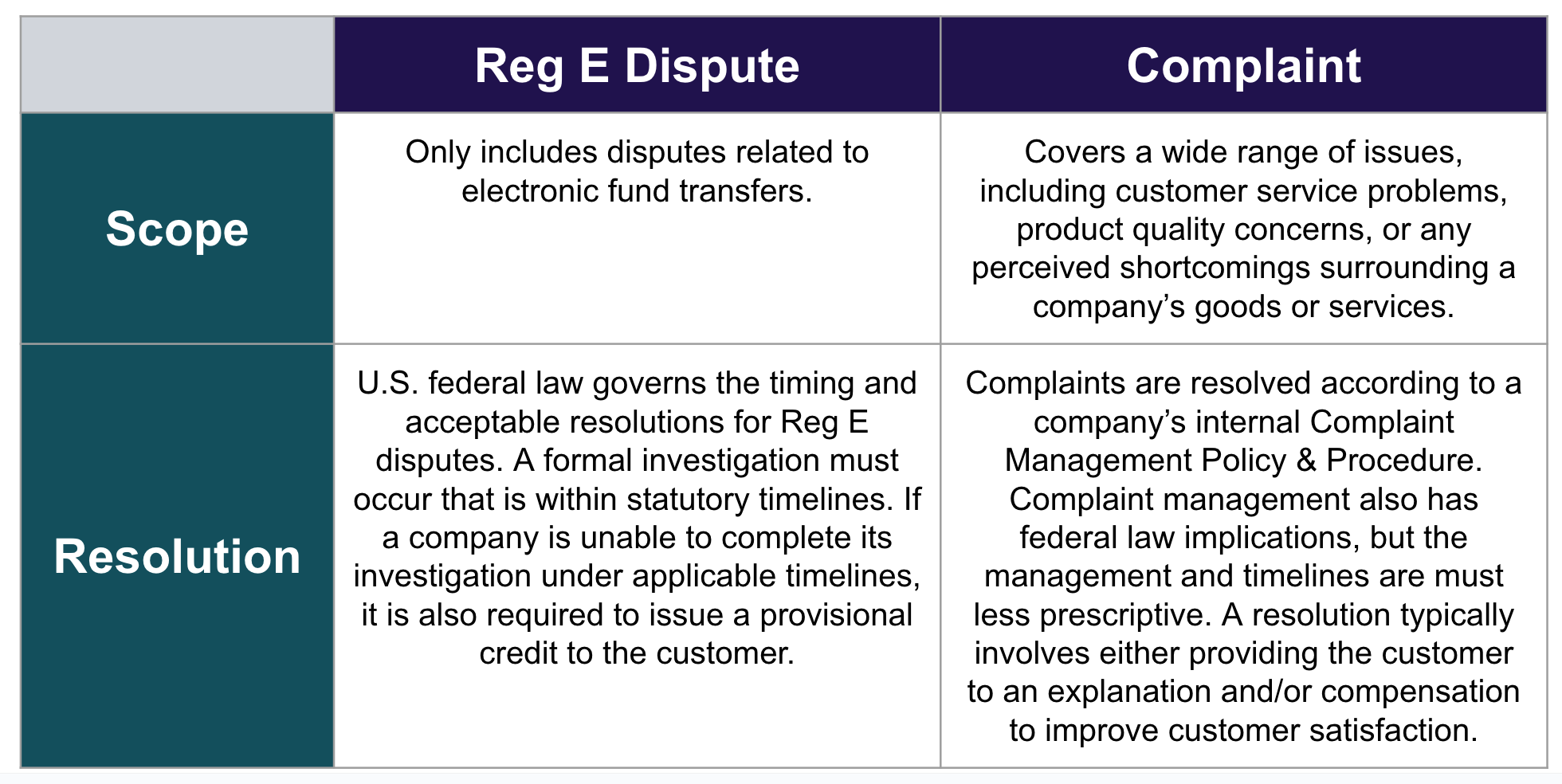

Reg E vs. Standard Complaints

At first glance, Reg E disputes can seem very similar to standard complaints. They differ in some fundamental ways in terms of scope and how they are resolved however:

Reg E dispute requirements

Under Reg E, consumers are entitled to receive provisional credit and financial institutions are not allowed to demand excessive requirements from them. The customer is only required to provide the following information:- Merchant name

- Transaction Amount

- Transaction Date

- Error Description

- Transaction Identifying Information has been provided

- Mention of Dispute Reason

- At least one (1) settled transaction

Exemptions from Reg E

Regulation E protects consumer electronic fund transfers, but not all errors fall under its scope. Please note that these are general examples, and specific details can vary. Transactions and errors outside the scope of Reg E include:- Returned Merchandise

- Merchandise/Service not Received

- Merchandise not as described

- Merchandise damaged/defective

- Canceled Merchandise/Service (one-time transaction)

- Errors Beyond the 60-day Timeframe

- Business/Commercial Transactions

CFPB Complaints Database

The CFPB Complaints Database is a publicly available database where companies can view and sort through complaints on financial companies and fintechs. This can be a useful way to see the types of complaints that may be emerging in your product type or industry. It also gives you a sense of what the CFPB may be tracking and what your Sponsor Bank partner will be focused on. Note that consumers can also directly make complaints about your Company via the CFPB so it is important that as part of complaint tracking, there is ongoing search of CFPB to check if there are any complaints about your business.Customer Communication

These templates are provided for your reference and convenience. It is the responsibility of the FinTech to communicate case updates and outcomes to customers. Always check the policies and procedures set by your Partner Bank, as Synctera only offers back-office support for disputes, and the FinTech, under the supervision of its Partner Bank, is responsible for front-line customer support and communication.Best Practices

- Except for fraud disputes, the customer should attempt to contact the merchant directly to resolve the issue. If the issue cannot be resolved, a dispute can be initiated.

- The disputed transaction must be posted to the customer account. A pending transaction cannot be disputed.

- Request supporting documentation, such as receipts or email communication with the merchant and timelines.

- When a card is reported lost, stolen, or compromised, immediately freeze the card to prevent unauthorized transactions.

| Notification | Description/Timing | Example |

|---|---|---|

| Acknowledgment | Promptly acknowledge the notice, provide details about any provisional credit, and explain the investigation process. | We are sorry to hear that your account contains a potential error. This message is to acknowledge the receipt of your dispute received [Date of Dispute Notice]. We will investigate your claim, and will provide a resolution once this matter has been fully investigated. We appreciate your patience and cooperation in this matter. |

| Provisional Credit | Provisional credit must be provided within 10 business days for established accounts and within 20 business days for new accounts. Notify about the provisional credit within 2 business days of issuance and that it is subject to reversal based on the outcome of the investigation. | While we continue to investigate your dispute, we have credited your account with the disputed amount of [disputed amount]. This is temporary credit that is effective as of [date of credit]. We will notify you of the outcome of our investigation by [date] at which time this provisional credit will either become permanent or be reversed depending on the outcome of the investigation. |

| Request Additional Info | When applicable, request more information or documentation to assist in the investigation. Provide clear instructions on what is needed and how to submit it. | We have begun investigating the transaction on your account dated [Transaction Date]; however, we need additional documentation or information, as noted below: [Information Needed to be Listed in Dispute Case]. Your prompt response will help us resolve this matter as quickly as possible. Failure to provide the requested information may impact the outcome of your claim. |

| Canceled Dispute | Promptly acknowledge the request, confirm that the investigation will end, and outline any actions taken or needed as a result. | We have received your request to cancel your claim regarding the transaction on your account dated [Transaction Date]. As requested, we have stopped our investigation, and we reversed the provisional credit of [$X.XX] on [Date]. |

| Resolution: Error Found - Provisional Credit Final | Notify the customer of the results within 3 business days. Provide details of the correction and confirm the final credit. | We have completed our investigation of the disputed transaction on your account and have determined that your claim is valid. The disputed amount of [$X.XX] has been permanently credited to your account. |

| Resolution: Error Found - No Provisional Credit, Final Credit Issued | Notify the customer of the results within 3 business days. Provide details of the correction and confirm the final credit. | We have completed our investigation regarding the claim on your account dated [Transaction Date] and have determined that your claim is valid. The investigation was completed before a provisional credit was due, therefore a final credit of the disputed amount of [$X.XX] has been permanently credited to your account. |

| Resolution: Error found - Merchant Refund, Provisional Credit Revoked | Notify the customer of the results within 3 business days. Provide details of the merchant refund, and confirm the date and amount of the provisional credit reversal. | We have completed our investigation regarding the claim on your account dated [Transaction Date]. Upon further review, we found that the merchant issued a refund for (amount) on [Date]. As a result of the merchant’s refund, the provisional credit of [$X.XX] will be debited from your account on [Debit Date]. |

| Resolution: Error Found - Merchant Refund, no Provisional Credit | Notify the customer of the results within 3 business days. Provide details of the merchant refund, and confirm that no provisional credit was issued. | We have completed our investigation regarding the claim on your account dated [Transaction Date]. Upon further review, we found that the merchant issued a refund for [$X.XX] on [Date]. As the refund was issued by the merchant, no provisional credit was provided during the investigation period. |

| Resolution: No Error - Provisional Credit Revoked | Notify the consumer of the results within 3 business days. Provide an explanation, disclose their right to request additional info, and promptly provide copies of the documents upon request. Include the date and amount of the provisional credit reversal, along with the fees for overdraft disclosure, 12 CFR 1005.11(d)(2). | We have completed our investigation regarding the claim on your account and have determined that no error occurred. The provisional credit of [$X.XX] will be debited from your account on [Debit Date]. We will honor checks, drafts, and similar instruments payable to third parties and preauthorized transfers from your account without charge to you as a result of an overdraft for five business days after this notification. You have the right to request additional information and documentation relied upon in making these determinations. |

| Resolution: No Error - No Provisional Credit | Notify the consumer of the results within 3 business days. Provide an explanation, disclose their right to request additional info, and promptly provide copies of the documents upon request and confirm that no funds will be credited to their account. | We have completed our investigation regarding the claim on your account dated [Transaction Date] and determined that no error occurred. As a result, a final credit was not issued to your account. You have the right to request additional information and documentation relied upon in making these determinations. |

Dispute Intake Questions

Asking targeted questions is crucial to uncovering factual information from customers. This helps remove ambiguity, obtain more details, and encourage customers to provide comprehensive answers. Documenting all relevant information in the case is important to fully understand the customer’s dispute. Here are some questions you can use based on the type of dispute.ATM Cash Dispute

The customer claims the ATM did not disburse funds. Documentation is required to help support the claim.- Have you contacted the merchant to resolve this issue?

- How much did you attempt to withdraw, and how much was dispensed?

- Did the ATM display any error message during the transaction?

- Do you have a receipt for this ATM transaction?

Card Lost, Stolen, or Never Received

The customer claims they did not have possession of the card.- When did you notice the card was lost, stolen, or not received?

- Have you previously reported this card as lost or stolen?

- When and where did you last make a legitimate transaction?

- Are there any other unauthorized transactions?

- Have you allowed anyone else to use the card? If so, have you checked with them?

- Do you have any documentation to help support this claim?

Chip Liability Shift

When a counterfeit card is used at a non-chip-enabled terminal, the merchant may be liable.- Did you use your card at a chip-enabled terminal for this transaction?

- Do you recall any issues or messages at the terminal?

- Have you attempted to resolve this directly with the merchant?

Counterfeit Goods

The merchant provided counterfeit items. Documentation is required to help support the claim.- How were the goods presented by the merchant?

- Do you have proof that the goods are counterfeit, such as an assessment or authentication?

- Have you attempted to resolve this directly with the merchant?

- Do you have proof of the order, such as a receipt or order confirmation?

Credit Not Received

The merchant promised the customer a refund not reflected on the account. Documentation is required to help support the claim.- Have you attempted to resolve this directly with the merchant?

- Why is the merchant processing a refund?

- Did the merchant confirm that a refund was processed?

- What date did the merchant process the refund?

- What amount was the merchant supposed to refund?

- Do you have proof of the refund, such as an email or receipt?

Defective Goods or Services

The merchant provided incorrect or faulty goods or services. Documentation is required to help support the claim.- Have you tried contacting the merchant to resolve this issue?

- What specifically was wrong with the goods or services received?

- Did the merchant offer a return, replacement, or refund policy?

- Do you have proof of the order, such as a receipt or order confirmation?

Dispute of Recurring Transaction

The customer claims they canceled, but the recurring charge continued, or they were unaware of the recurring agreement. Documentation is required to help support the claim.- Have you tried contacting the merchant to resolve this issue?

- Did you request that the merchant cancel the recurring transaction?

- Do you have a confirmation of the cancellation request?

- Were you informed of a recurring charge when you initially signed up?

Duplicate Transaction

The customer only made one transaction and was charged more than once. For this reason, the transactions must have been made on the same day. Documentation is required to help support the claim.- Have you tried to contact the merchant about the duplicate charge?

- How many times was your account charged for the same transaction?

- Were the charges posted on the same date?

- Do you have a receipt or proof of the original transaction?

Fraudulent Processing

The customer has multiple charges at the same merchant but only authorized one transaction. Documentation is required to help support the claim.- Have you conducted any recent face-to-face transactions with this merchant?

- Were you in possession of your card during these transactions?

- Have you tried contacting the merchant to resolve this issue?

- Has the merchant addressed any issues with processing multiple transactions?

Goods or Services Not Provided

The merchant did not provide goods or failed to fulfill services. Documentation is required to help support the claim.- When was the product or service supposed to be delivered?

- Have you contacted the merchant to resolve this issue?

- Do you have proof of the order, such as a receipt or order confirmation?

Late Presentment

The transaction was delayed in processing, leading to an unexpected charge days or weeks later.- Have you contacted the merchant to resolve this issue?

- Do you recall authorizing this transaction on a different date?

- Did the merchant inform you of any delays that may have affected this charge?

Paid by Other Means

The customer used a different form of payment for this specific transaction. Documentation is required to help support the claim.- Have you contacted the merchant to resolve this issue?

- What alternative payment method did you use for this transaction?

- Do you have a receipt showing the use of the other payment method?

Transaction Amount Differs

The customer authorized a different amount than the settled amount. Documentation is required to help support the claim.- What was the amount you expected to be charged?

- What was the amount you were actually charged?

- Have you contacted the merchant to resolve this issue?

- Do you have an invoice or receipt showing the agreed-upon amount?

Transaction Did Not Complete

The customer participated in the transaction, but it failed to complete due to a system error or merchant issue. Documentation is required to help support the claim.- Have you contacted the merchant to resolve this issue?

- Did the merchant confirm the transaction and provide a receipt?

- Were you notified of any transaction errors?

Transaction Not Recognized

The customer does not recognize the transaction due to an unclear merchant descriptor.- Do you recognize the merchant’s name or location listed?

- Could this transaction be part of a subscription or recurring payment?

- Have you reviewed any similar transactions that might clarify?

- When and where did you last make a transaction that you recognize?

- Do you have your card, or is it lost/stolen?

- Have you allowed anyone else to use the card? If so, have you checked with them?

- Do you have any documentation to help support this claim?

Unauthorized Transaction

The customer was not involved in the transaction and claims fraud.- Did you authorize or recognize this transaction?

- When and where did you last make a legitimate transaction?

- Do you have your card, or is it lost/stolen?

- Have you allowed anyone else to use the card? If so, have you checked with them?

- Do you have any documentation to help support this claim?