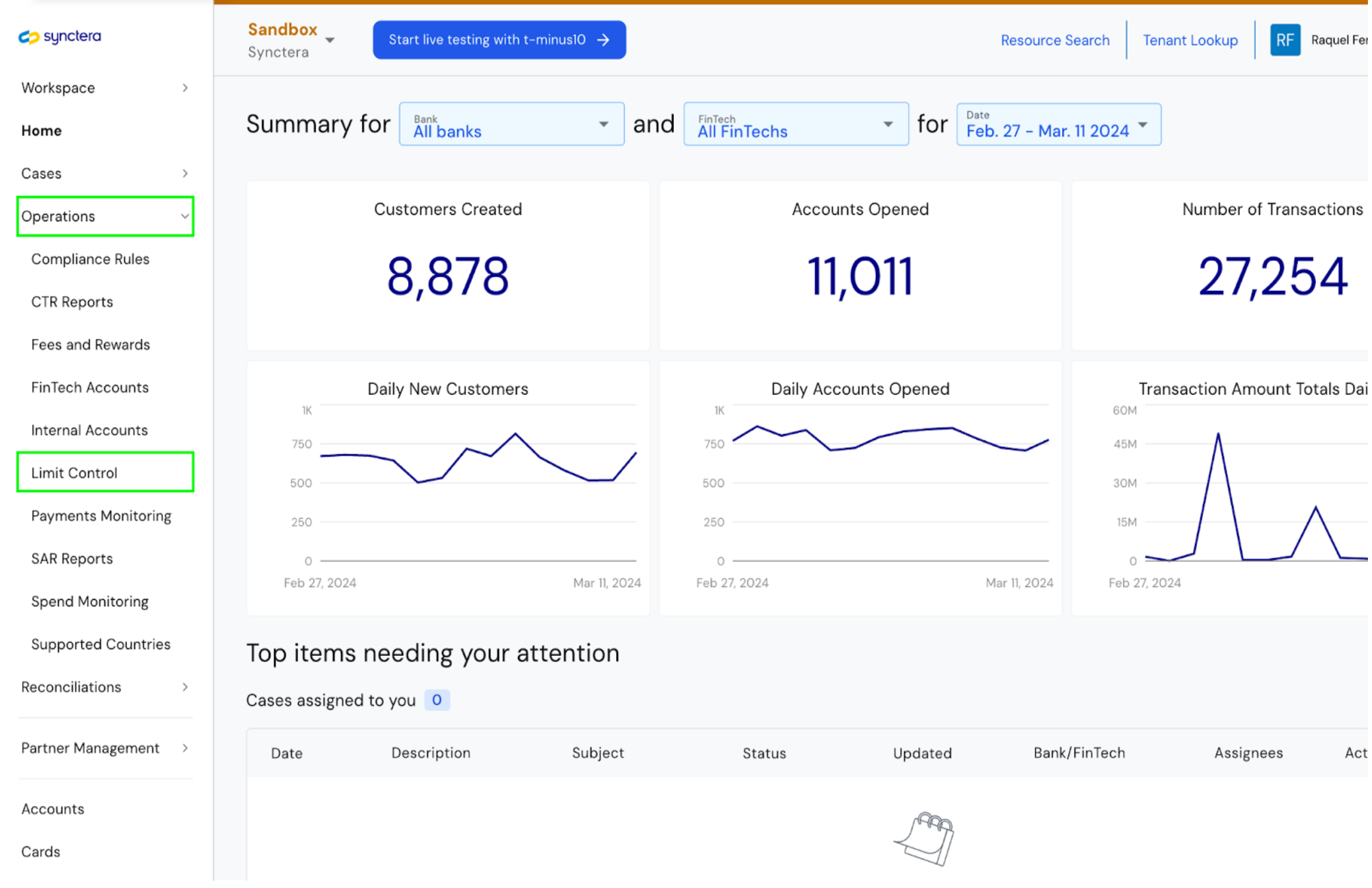

Limit Controls:

Limit Controls are FinTech-Level daily limits that can be set by the Bank and Synctera Risk Operations to manage a daily transaction amount of Outbound ACH Debits and Outbound ACH Credits for a FinTech. These limits are specially designed for Banks to manage their liquidity risk, i.e if a FinTech sends a large amount of Outbound ACH Debits (pulls) then there is a risk of return for 2 business days, the bank wants to manage this as well as their liquidity risk in their Fed account for ACH. If the Fed account is overdrawn, then the bank needs to pay interest to the Fed. By managing this risk at the FinTech Level, they can adjust the daily transaction amount from the UI and forecast the available transacting funds for a specific FinTech.This feature is only available for ACH at the moment, other FinTech-specific limits are currently set in Feedzai and Marqeta for card transaction limits.

Who can create and update limit controls?

- The Bank Operations teamcan create, view and update FinTech-Level Limits

- The Synctera Risk Operations team can create, view and update FinTech-Level Limits

- The FinTech OPS team can view only their FinTech-Level Limits

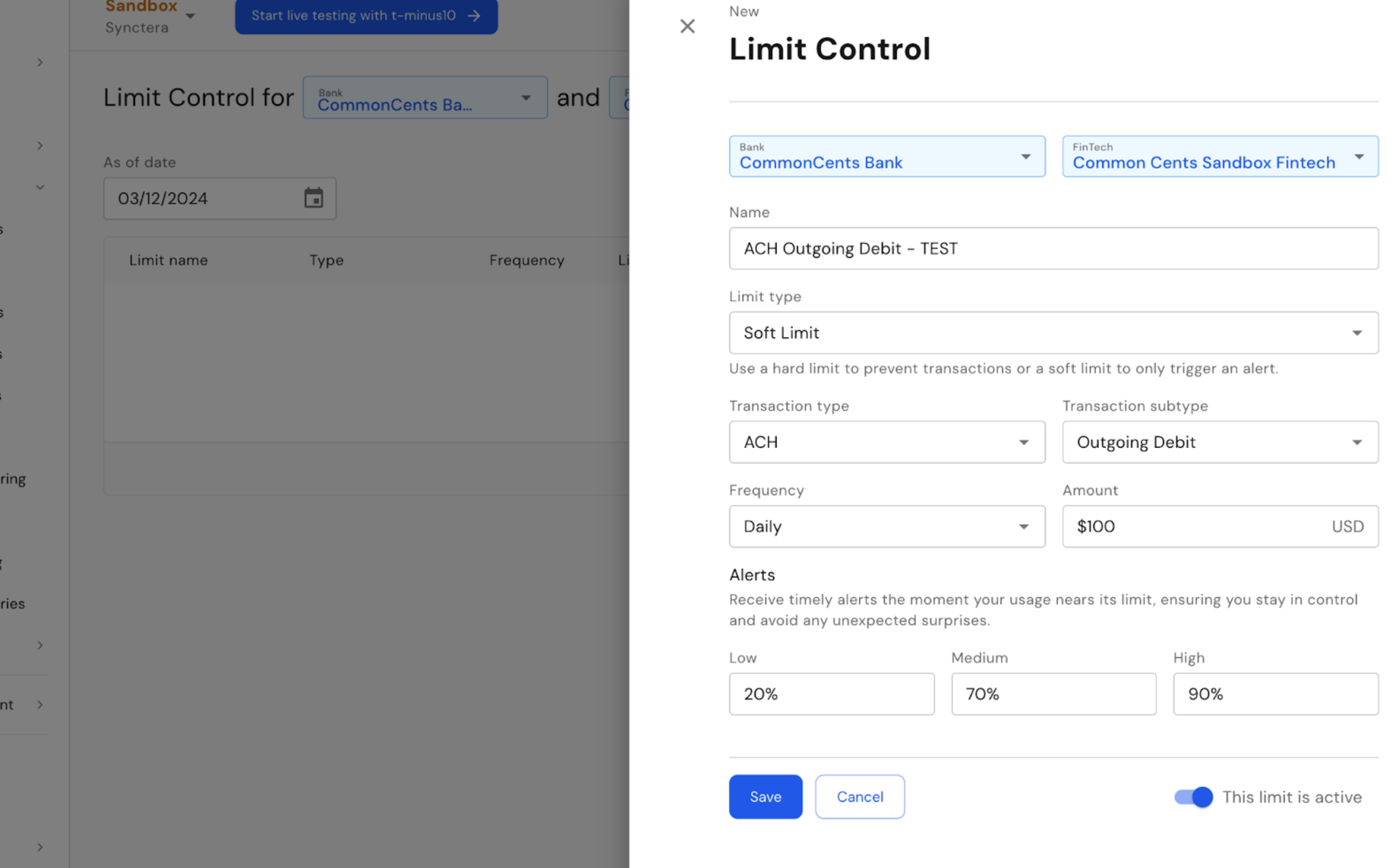

How to setup a FinTech-Level ACH limit:

- Name: Free text field, create your own name to identify the limit

- Limit type:

- Soft limit: will create a notification when the daily limit is reached for the FinTech OPS to communicate with Synctera OPS and the Bank to update the daily limit. This limit being reached doesn’t stop the FinTech from transacting

- Hard limit: will create a notification when the daily limit is reached for the FinTech OPS team and stops the FinTech from transacting with ACH until the Bank OPS or the Synctera OPS team updates the limit

We recommend to first setup Soft Limits to test the feature and workflows with the FinTech, hards limits can provide a bad fintech customer extperience as the transaction is declined when the FinTech reaches their daily limit

- Transaction type: ACH

- Transaction subtype: Outgoing Debit (pull) and Outgoing Credit (push)\

- Frequency: daily

- Amount: This is the daily amount for that specific sub-type

- Alerts: The Bank can set limit utilization alerts based on risk. For example 20% utilization is considered low risk, 70% utilization is considered medium risk and 90% utilization is now considered high risk. This is all configurable and the bank can create their own definition of low, medium and high risk

- This limit is active toggle: Bank can activate the limit right away or later. Use the activate toggle.

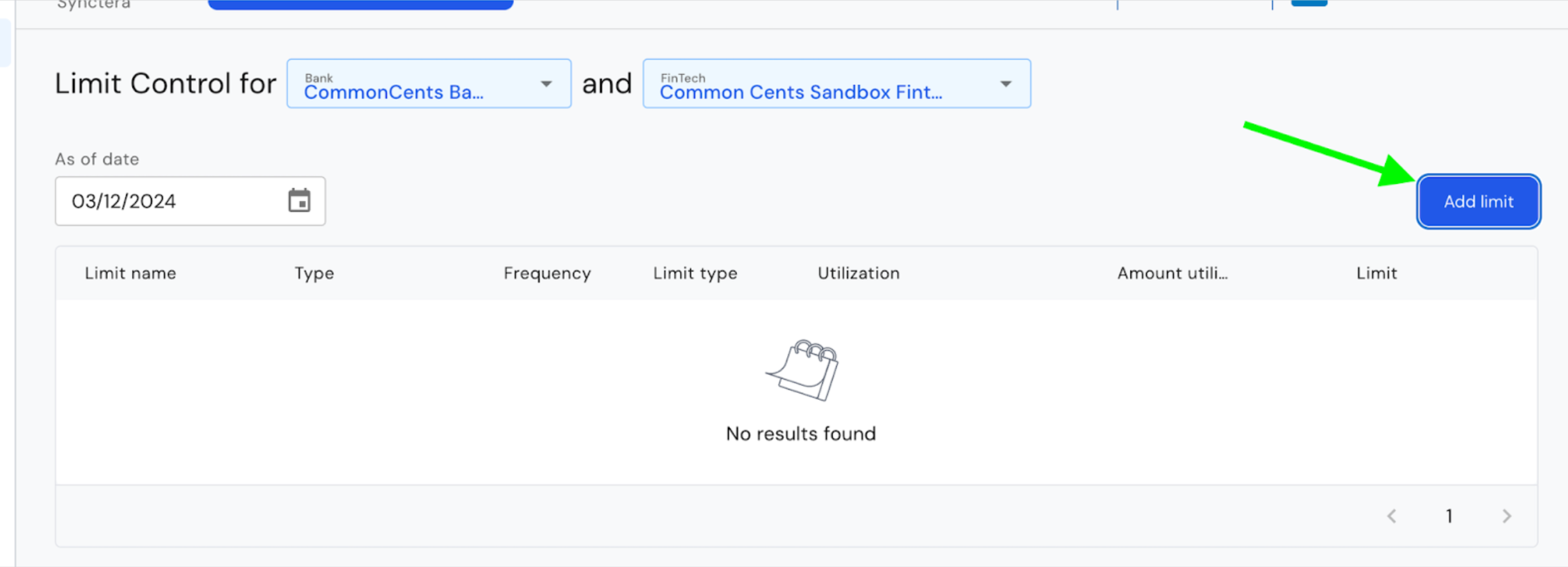

How to manage and monitor limits:

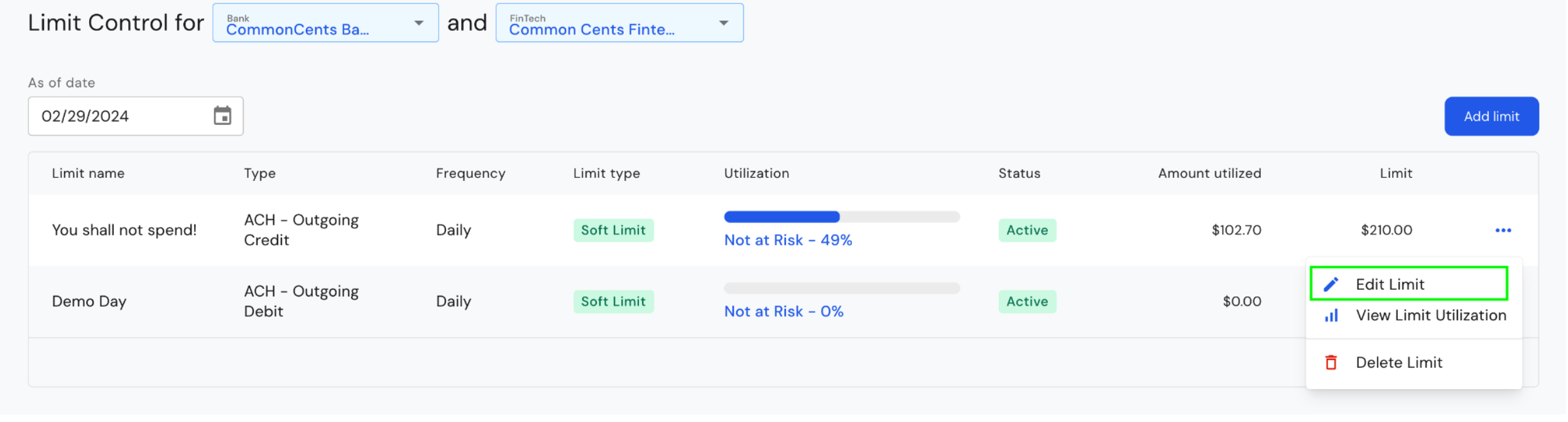

After a limit is created, it can be managed via the Limit Control UI.- Banks and Synctera OPs can view and modify limits

- FinTechs can only view limits and cannot edit the limit

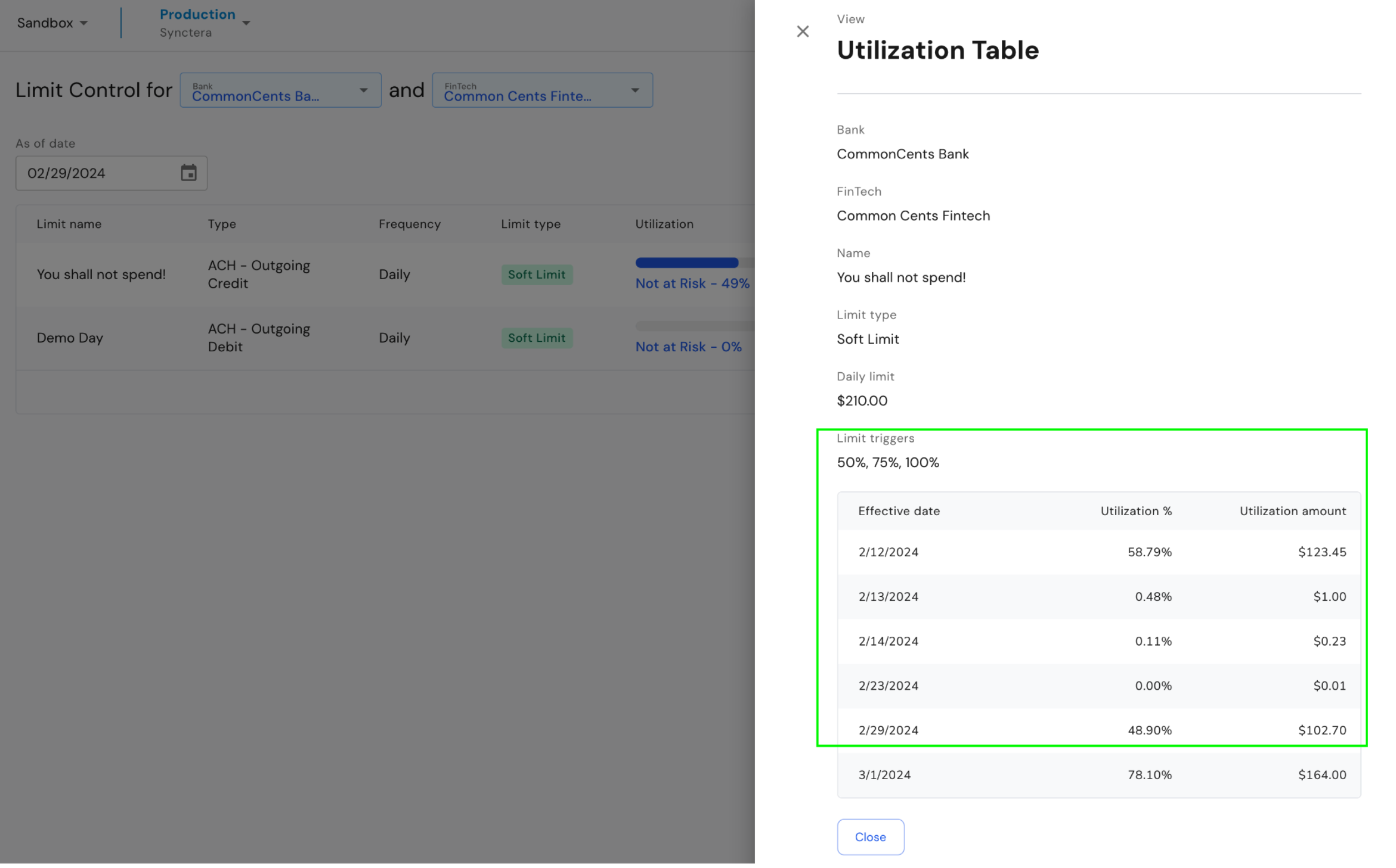

- The limit utilization is calculated based on the ACH transaction effective date.

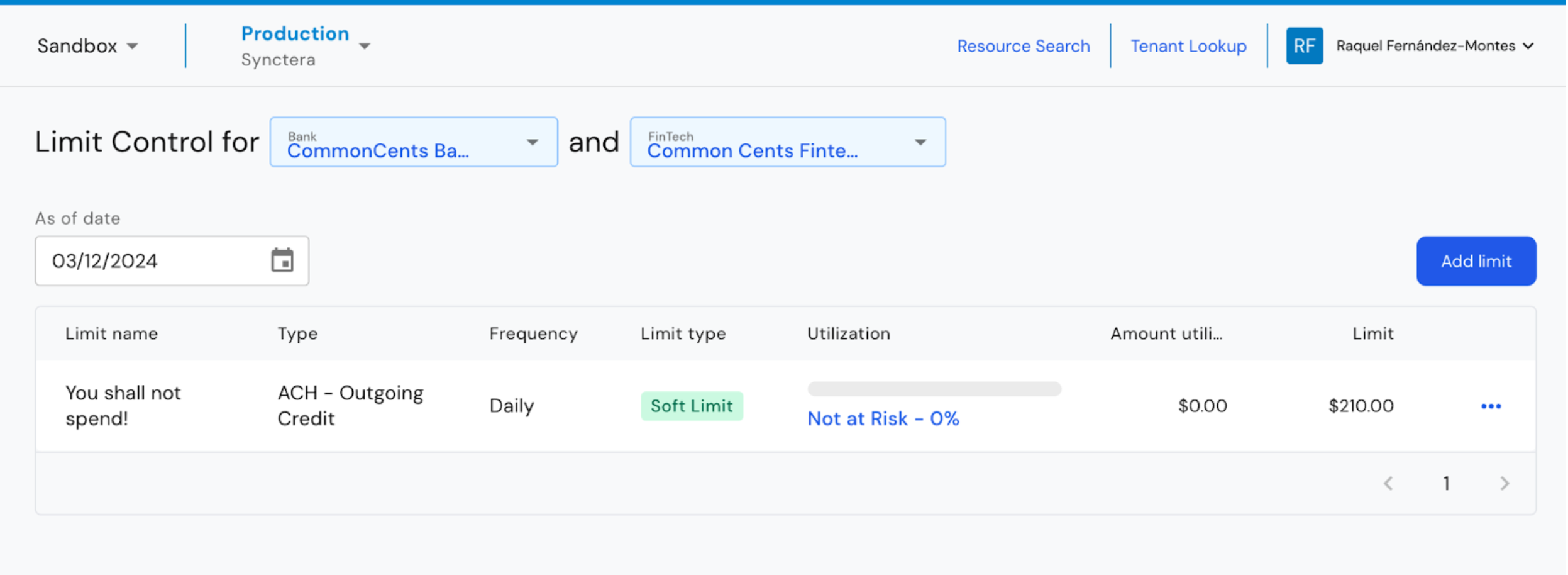

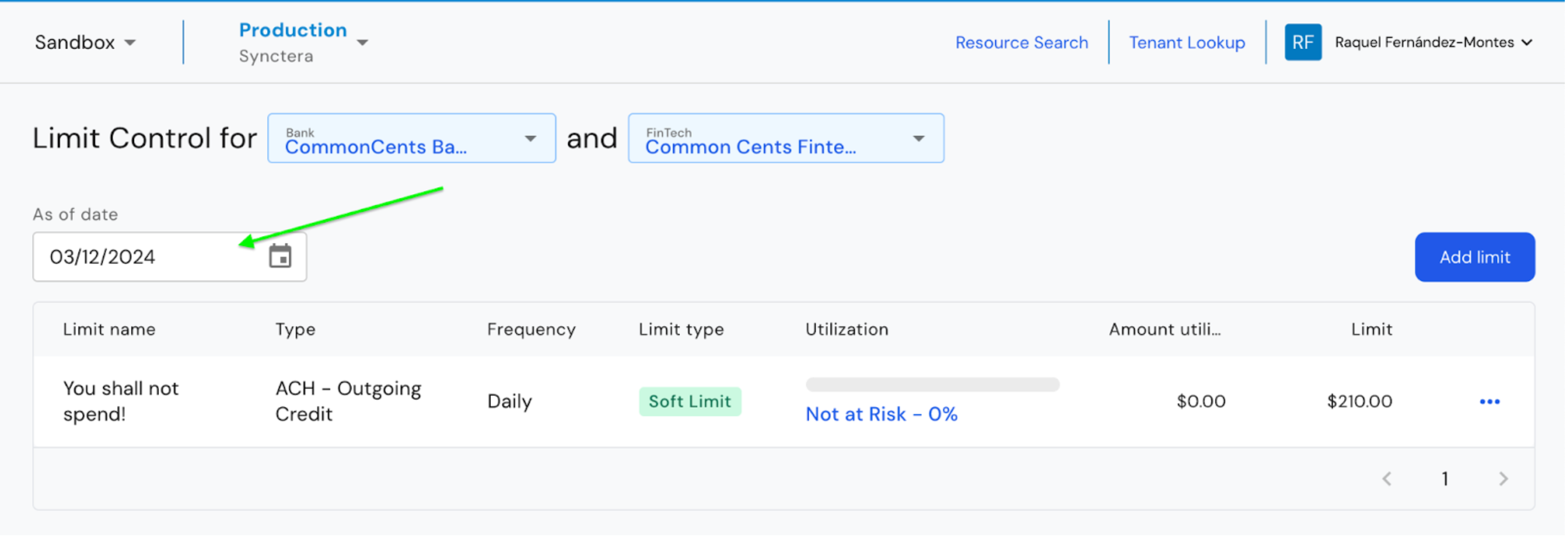

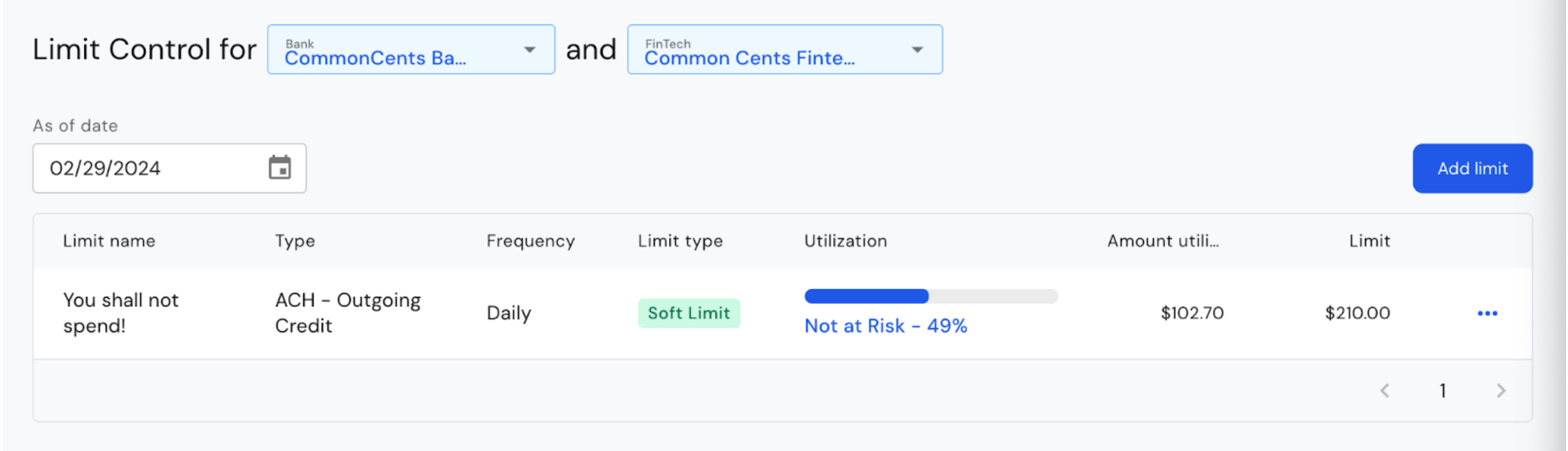

- One of the most important parts of the UI is the ‘As of date’ date picker

- By choosing a ‘as of date’ date, we can see the utilization for that specific ‘EFFECTIVE DATE’. As mentioned in this guide before, the utilization amount is calculated based on the transaction effective date (see utilization bar increasing when picking up a new effective date)

Monitoring utilization and updating the daily limit:

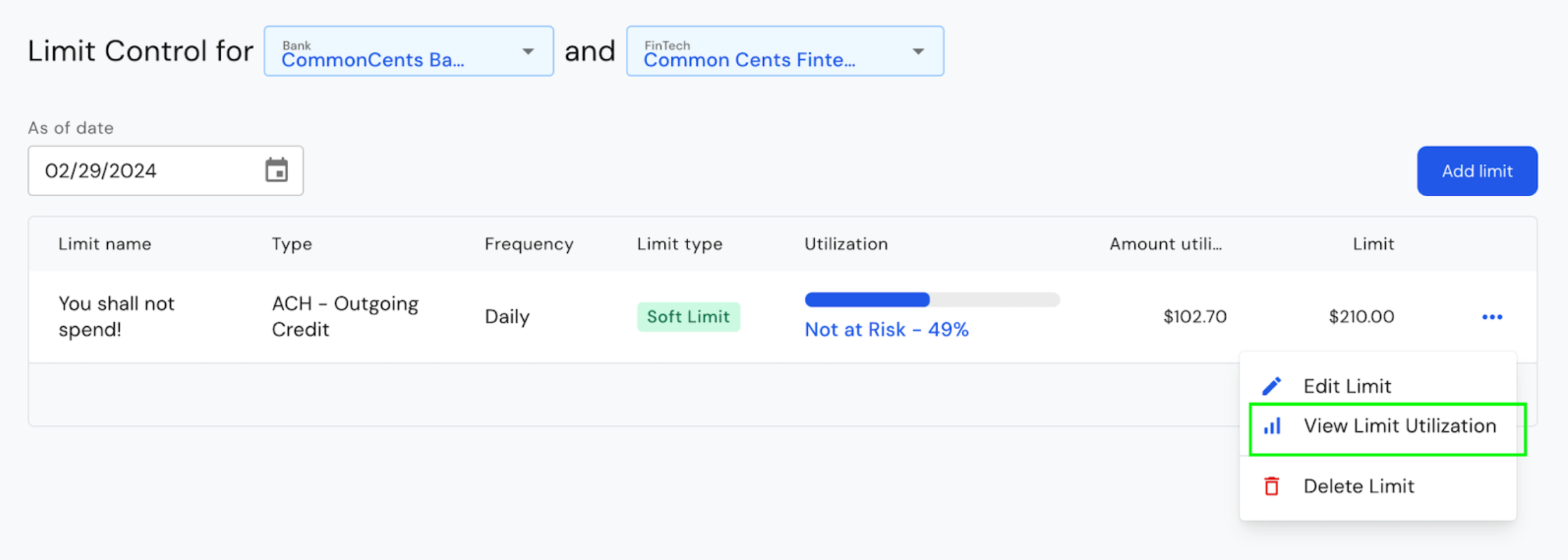

- Go to the 3 dots at the end of the limits table UI and click on ‘View limit utilization’

- The utilization table, based on the transaction effective date shows up on the UI

- The daily limit can be updated. Click on ‘Edit Limit’

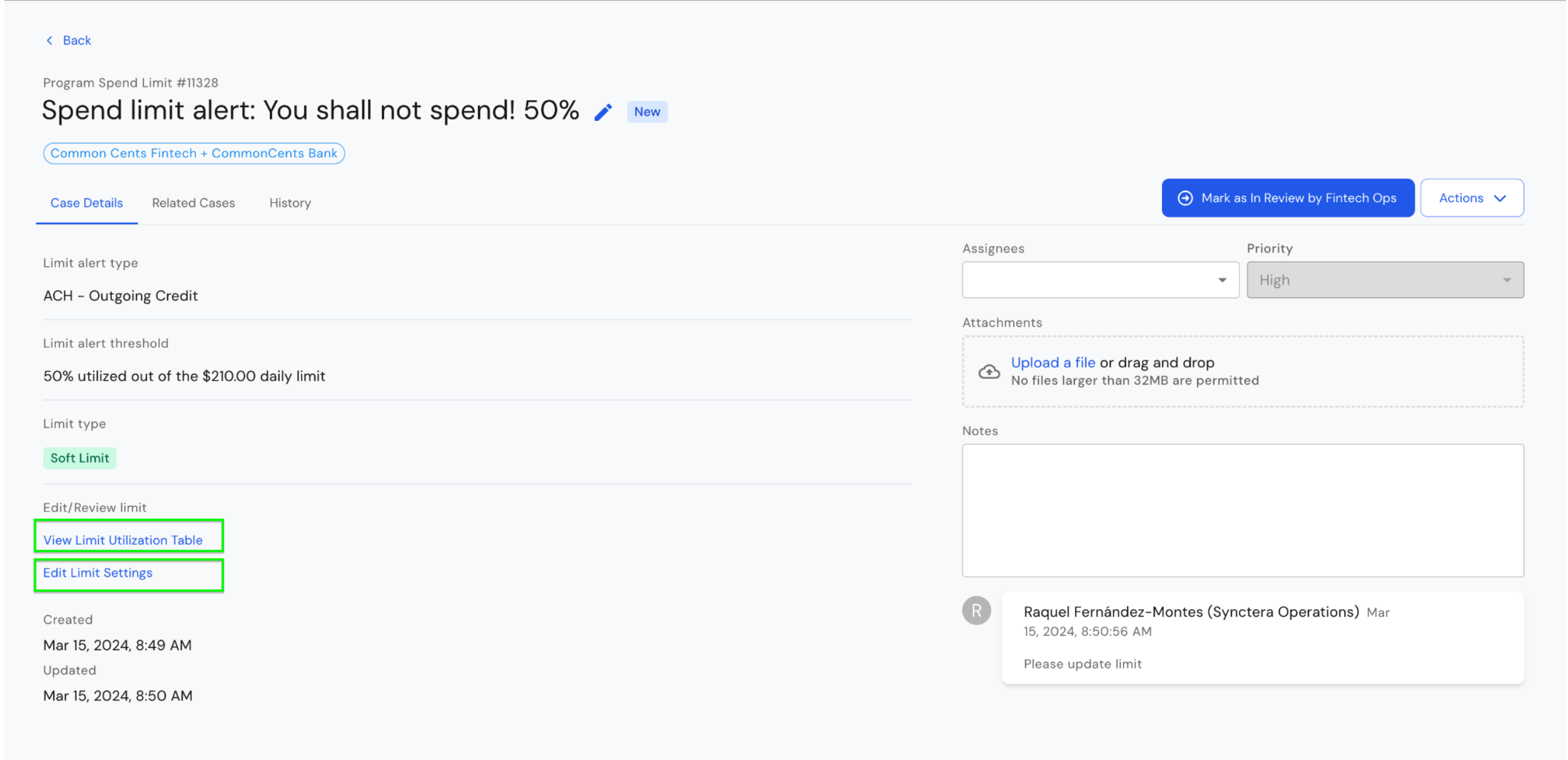

Limit Control Cases:

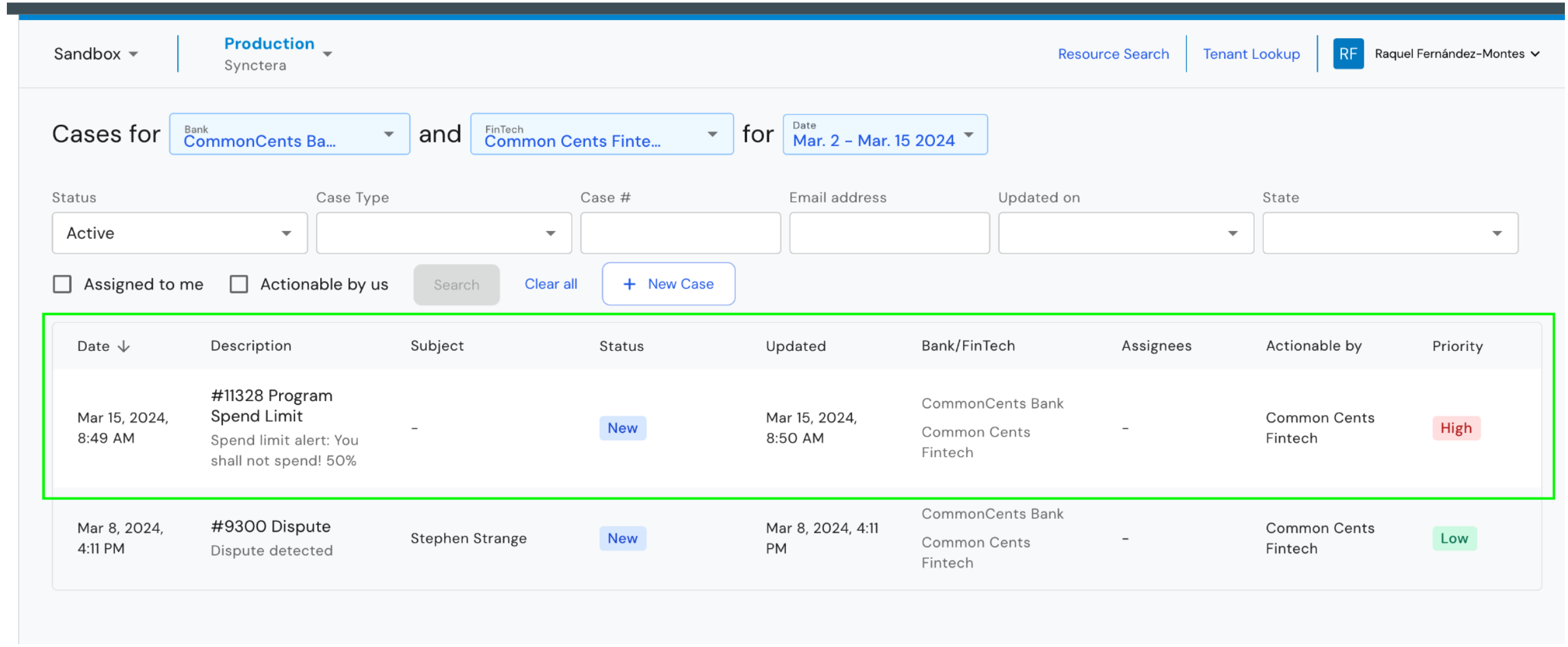

You can set notifications alerts when you create the limit. For example the Bank can set up case notifications at 20% , 70% and 90% utilization. Additionally, cases will be always created when the FinTech reaches 100% of the limit utilization.Cases workflow:

- Case is created, the case is assigned to the FinTech Operations team and Synctera Operations is informed.

- If the limit needs to be updated, the FinTech Operations team adds a comment to the case and assigns the case to the Bank Operations team. Synctera is informed in this process

- The Bank Operations team, updates the limit, adds comment with the change and closes the case.

- If the limit doesn’t need to be updated, FinTech can close the case with a comment

Cases UI:

- Cases for Limit Control are in the Cases UI as ‘Program Spend Limit’

- Bank Users and Synctera Risk OPS can review the limit utilization table and edit the Limit Settings from the UI