SyncteraPay: Product Overview

What is SyncteraPay?

SyncteraPay allows FinTechs to process payments with their Third Party payments providers. As a result, the payment transaction is stored in the Synctera Ledger with all the relevant payment information (network reference ID, sender, recipient, FX conversion, ect…) All of this information is needed for compliance and account statements.What is the value of SyncteraPay for the FinTech and the Bank?

FinTechs can bring their own partners into the Synctera platform and settle payments with them (i.e bring Stripe for OCT or TransferWise) or they can find a partner outside the Synctera Markeplace that they like moreHow does Synctera facilitate the SyncteraPay implementation?

- FinTech brings their Third Party Payments provider and use case (i.e international remittance, OCT, check issuing, ect…)

- Synctera compliance works with the Bank and the FinTech to go through the Third Party Risk assessment process and approve the proposed flow of funds. As a result the Thrid Party provider vendor is approved and stored in the Synctera Platform.

- Synctera and Bank setup the required data needed for a compliant integration (i.e sender name, country, account number, ect)

- Onboarding in the platform in PROD by I&O

- Help to set up the bulk settlement accounts for Third Party Settlement

- Fraud management and OFAC checks with Bank and Synctera compliance

- Settlement and Operational processed covered with the Bank

- Compliance Reporting and oversight

- Transaction Reconciliation

- Transaction Reporting

How does SyncteraPay work?

High-Level business process to send funds:

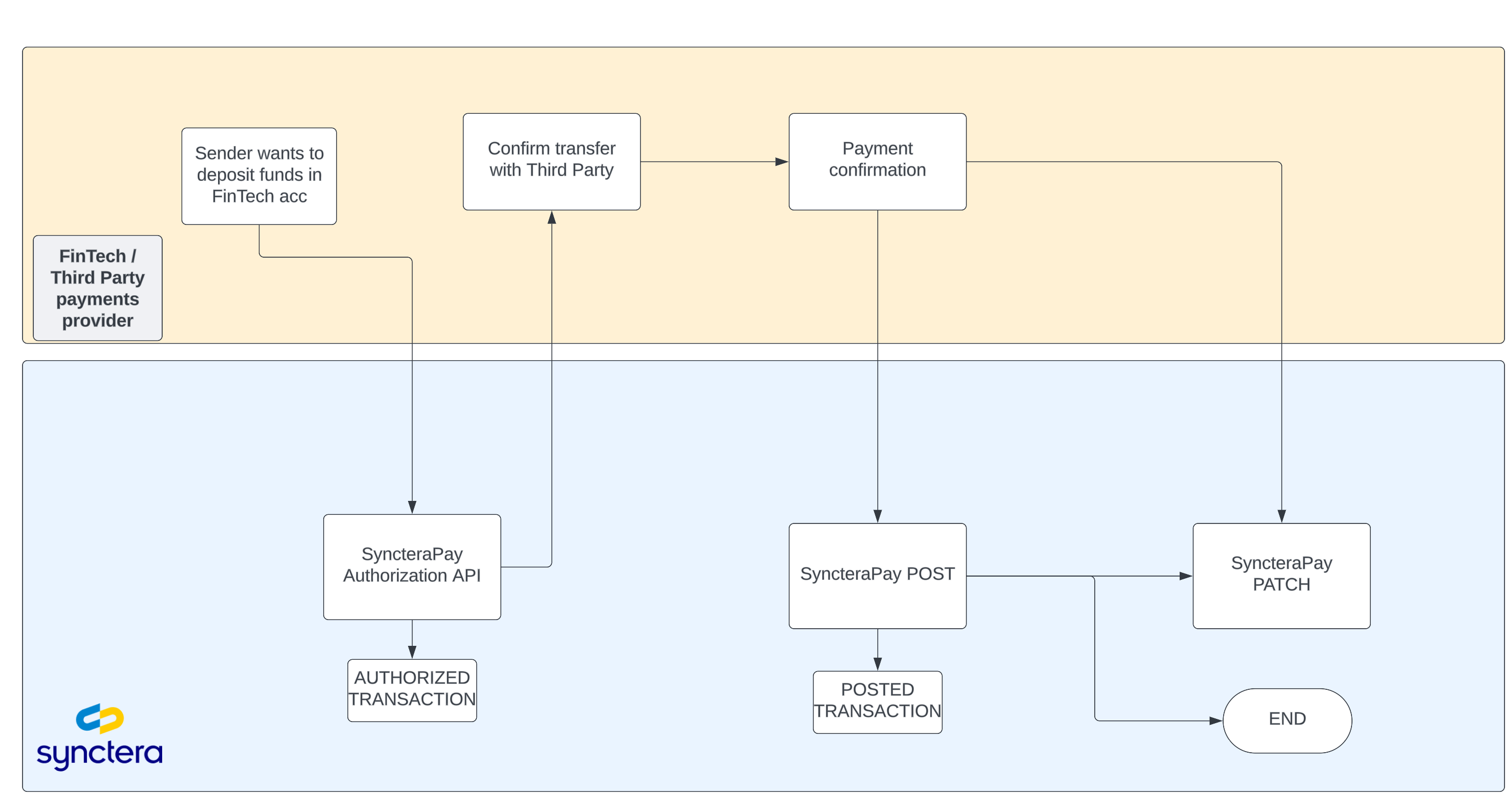

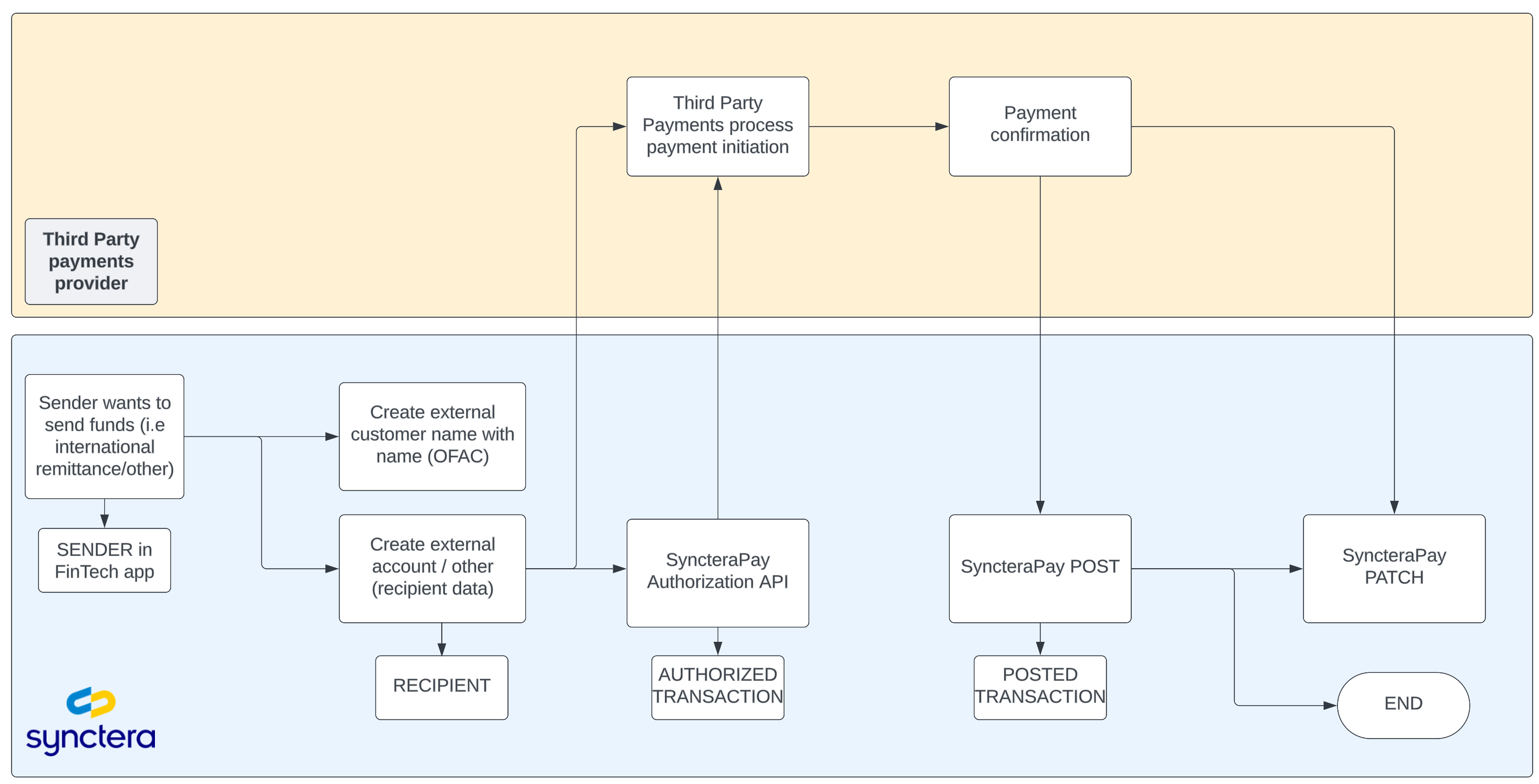

- FinTech customer wants to send funds in FinTech app via a third party provided (i.e TransferWise)

- FinTech creates a beneficiary name and beneficiary account in the Synctera Platform

- FinTech communicates instructions to third party payments provider and initiates a transaction authorization to the customer via the SyncteraPay ‘CREATE transfer’ API. The authorization validates the account status and runs OFAC and Fraud checks. If the authorization is successful, then the transaction can be confirmed with the third party payments provider.

- FinTech confirms transfer with Third Party payments provider and confirms authorization by calling the ‘UPDATE SyncteraPay’ API.

- FinTechs can UPDATE the SyncteraPay transaction amount, and transaction metadata after the transaction is posted.

High-Level business process to receive funds:

- FinTech receives funds from a Third Party Provider

- FinTech initiate authorization to validate account details, status and fraud checks calling the ‘CREATE transfer’ API. If authorization is successful, FinTech confirms transfer with third party payments provider.

- FinTech calls ‘UPDATE SyncteraPay transfer’ after confirming transfer with third party payments provider. This confirms the transfer.

- FinTechs can UPDATE the SyncteraPay transaction amount, and transaction metadata after the transaction is posted.