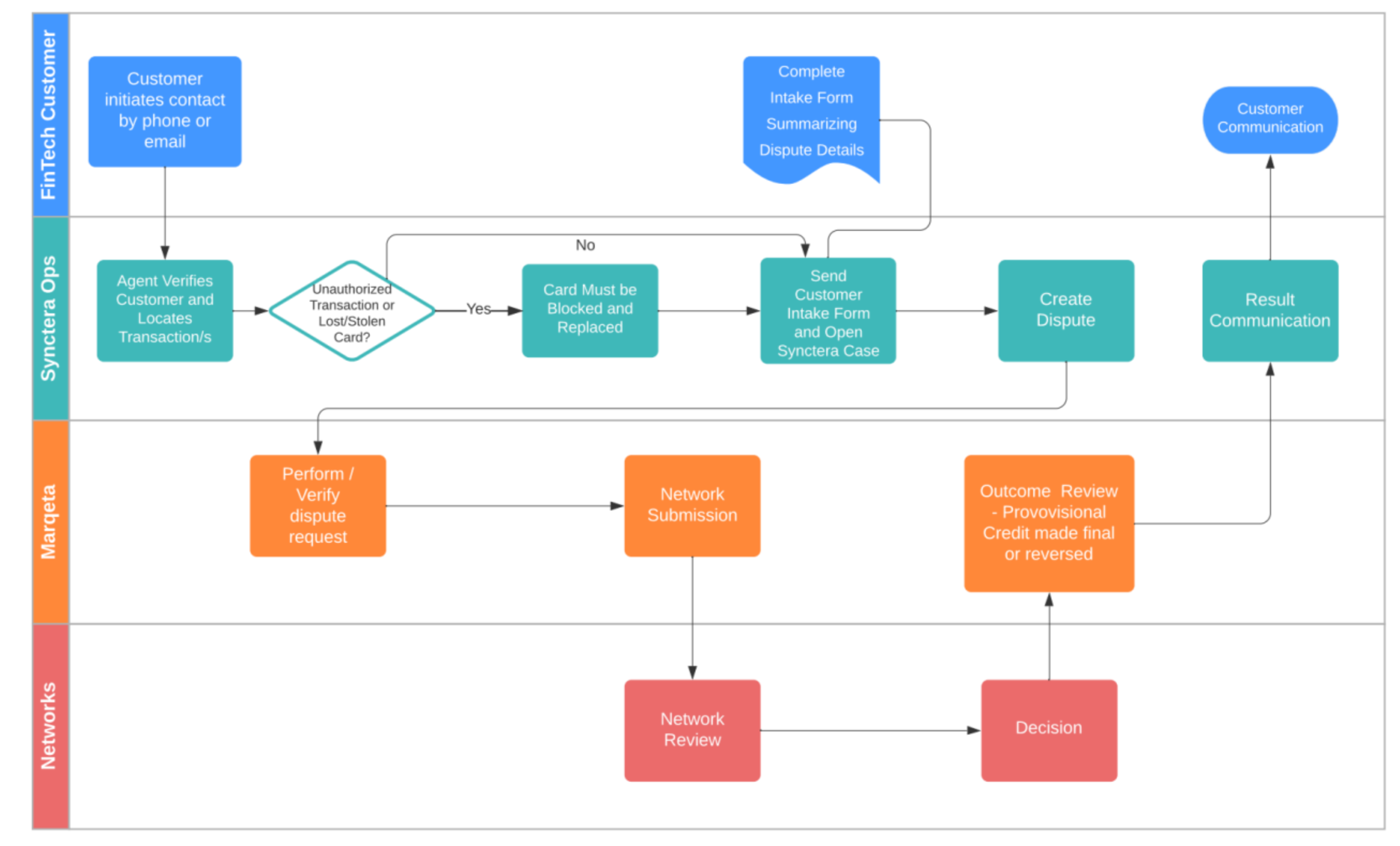

Overview

Anytime a customer disputes a transaction made on their card or their account, a Dispute Case can be created to track the lifecycle and events that take place during investigation into the dispute, including provisional credit amounts and final outcomes.When to use the Dispute case type

Dispute Cases should be created manually anytime a customer notifies the FinTech that they’d like to dispute a transaction, whether the notification is via phone call, email, or other means in the FinTech’s application. This case will track dates and actions taken around disputes like when the dispute was opened and when the investigation must be completed by, when provisional credit was provided and what the amount was, and what the final outcome of the dispute investigation was.What’s displayed for Dispute cases

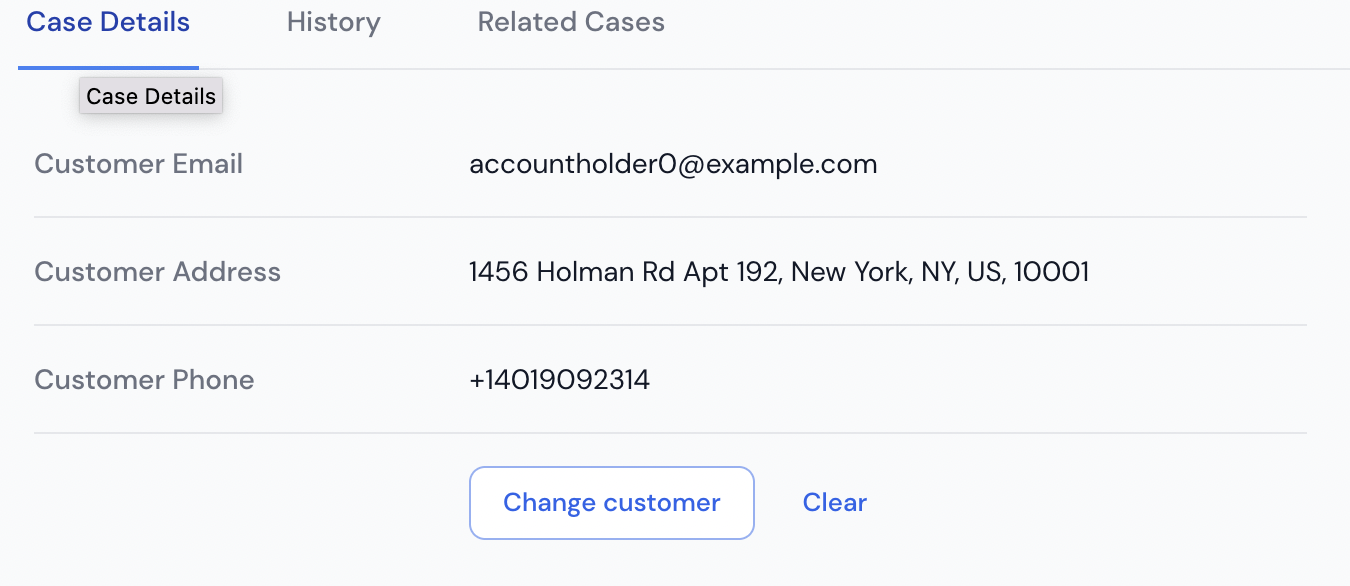

Customer information

A quick overview of the customer with a link to the Customer Info page with further details about the customer. Users can select the related customer by searching using their Customer ID.

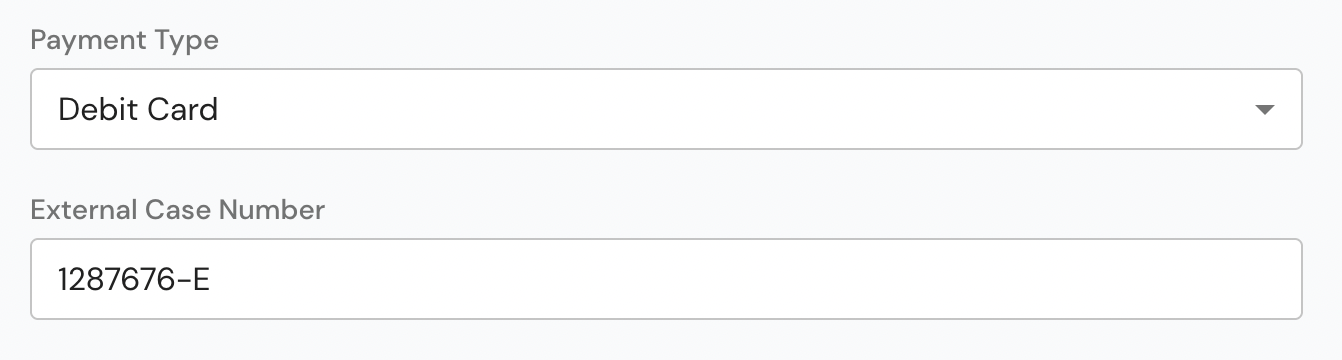

Payment type

The type of Dispute case to open. In most cases this will be a Debit Card dispute.External case number

Used for linking this Synctera case to any other case systems where disputes are also being tracked and investigated, like Marqeta.

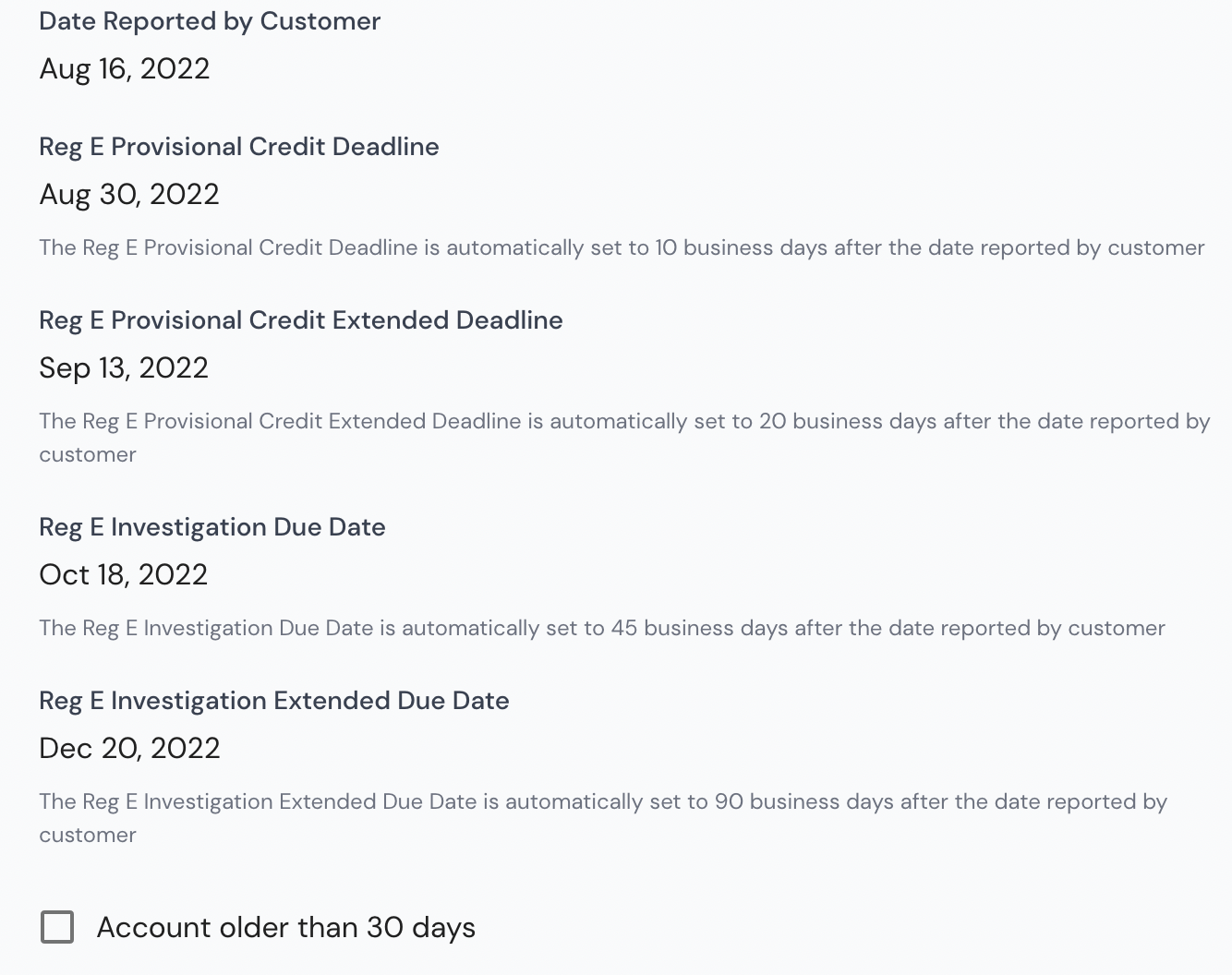

Date reported by customer

The date the customer contacted the FinTech to dispute the transaction. This is used to calculate due dates for provisional credit, investigation completion, and other Reg E related dates. This defaults to the date the case was opened.Due dates

The dates that certain aspects of the investigation must be completed by in order to meet Reg E timelines. Specifically the standard and extended Provisional Credit Deadlines, and the standard and extended Investigation Completion Deadlines. These are auto calculated based on the Date Reported by the Customer.

Account identifier/number

Used to note which account the transaction being disputed occurred in, in case there is need to investigate the transaction history of the account to compare similar transactions.Transaction identifier/number

Used to note the specific transaction that is being disputed.

Provisional credit info

Used to store the date and amount of any provisional credit provided to the customer, and if required, the date and amount of that provisional credit that was reversed at the final outcome of the investigation.

Final message date

Used to note the last contact date with the customer. Used to note when the final message with the customer was, to ensure and have proof of compliance with Reg E timelines.

Dispute amount

Used to store the amount the customer is disputing on the transaction. The dispute may be the entire amount of the transaction or only some part of the transaction.Merchant name

Used to store the name of the merchant the disputed transaction occurred at.

Card ID

Used to store the card identifier, which can be found under the Customer Info page for the customer by looking at their related cards.Card status

Whether the card is within the possession of the customer or not.Card last 4

Used to store the last 4 digits of the card number, gathered from the customer if the card is still in their possession, or from the Card Info page for cards connected to the customer.Card expiration date

Used to store the expiration date of the card used in the disputed transaction, gathered from the customer if the card is still in their possession, of from the Card Info page for cards connected to the customer.

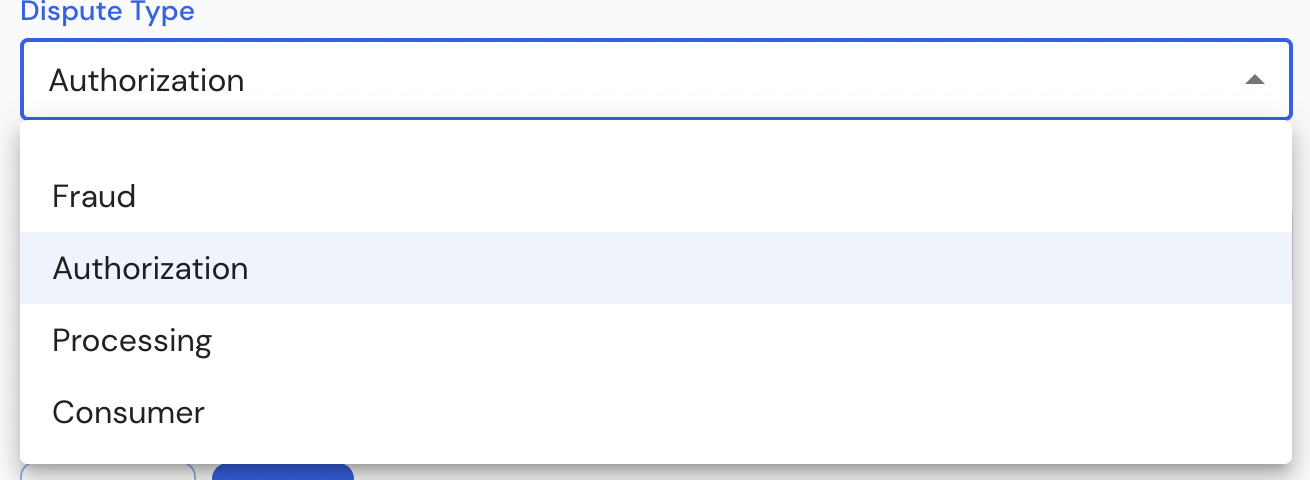

Dispute type

The specific type of dispute the customer is opening, based on defined network dispute types (Fraud, Authorization, Processing, or Consumer).

Reviewing and decisioning cases

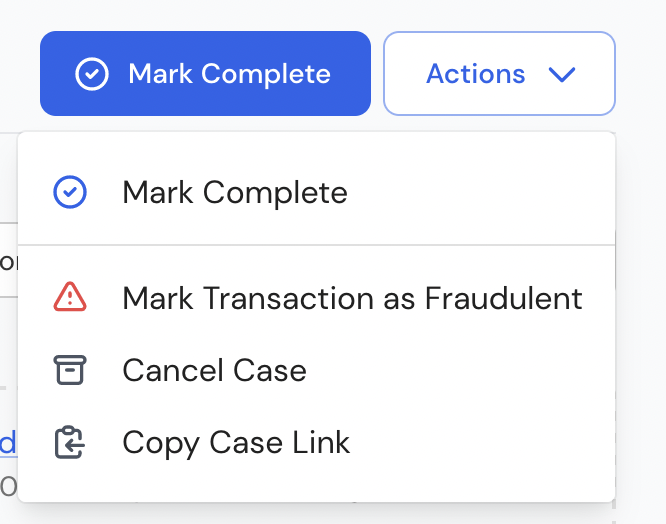

Cancel case

In the scenario where the customer would like to cancel a dispute, the case can be cancelled as well.Submit case

Take this action when all of the initial information about the dispute has been gathered and entered into the Synctera Console. From there, the information will be relayed to Marqeta, who will be performing the investigation at the network level and providing updates and possibly requests for further information or documentation from the customer that opened the disputeMark complete

Take this action when a final decision has been made on the dispute and credit has been provided. This is a terminal state, and should be used when the dispute has been either confirmed as valid or not valid. Once the case is put into this state there can be no further action taken.Mark transaction as fraudulent

Take this action when it is determined by the investigation that the transaction being disputed was in fact fraudulent. This will update the transaction fraud model and notify it that the transaction was fraudulent, helping the model to learn that those types of transactions for a the customer should be considered fraud going forward.Roles & Responsibilities