Introduction

Fedwire is a real-time gross settlement (RTGS) funds transfer system operated by the U.S. Federal Reserve Banks. It’s typically used by financial institutions and businesses for large-value or time-sensitive transactions. Payments are initiated by a sender and passed through the wire network to a receiver (push payment).Wires exchange with Synctera

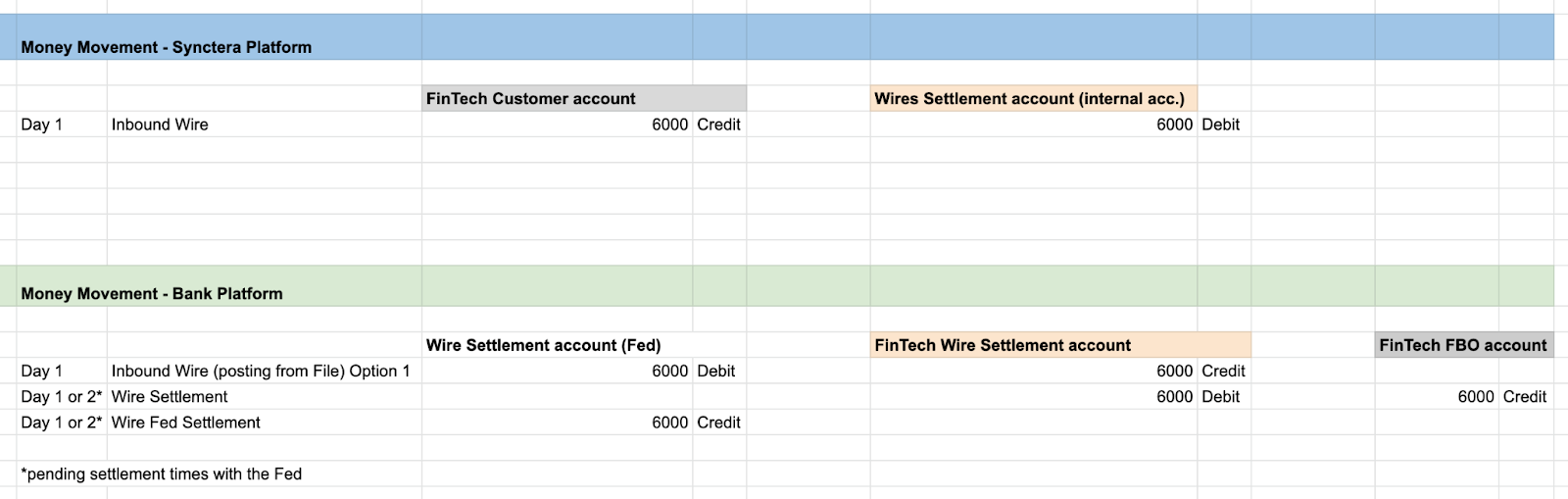

Inbound file processing (From Fed to Sponsor Bank)

The Sponsor Bank receives inbound wire transfers files multiple times a day. The credits and debits (returns) are posted against the Bank customer accounts. When Wires need to be posted to the FinTech accounts in Synctera, the sponsor bank needs to redirect those payments to Synctera.Wire file from FedWire is redirected to Synctera.

The process is as follows:- The bank receives an incoming wire from the Fed, on the Synctera ABA

- The bank downloads the file, and uploads it to the Synctera SFTP

- Once file is sent via SFTP, Synctera will automatically ingest the file

- Syntera runs transaction checks for the transaction (OFAC, AML, etc.)

- FinTech customer account is credited

- Posting entries for the wire will be generated same day, and sent via the normal autosweeps file

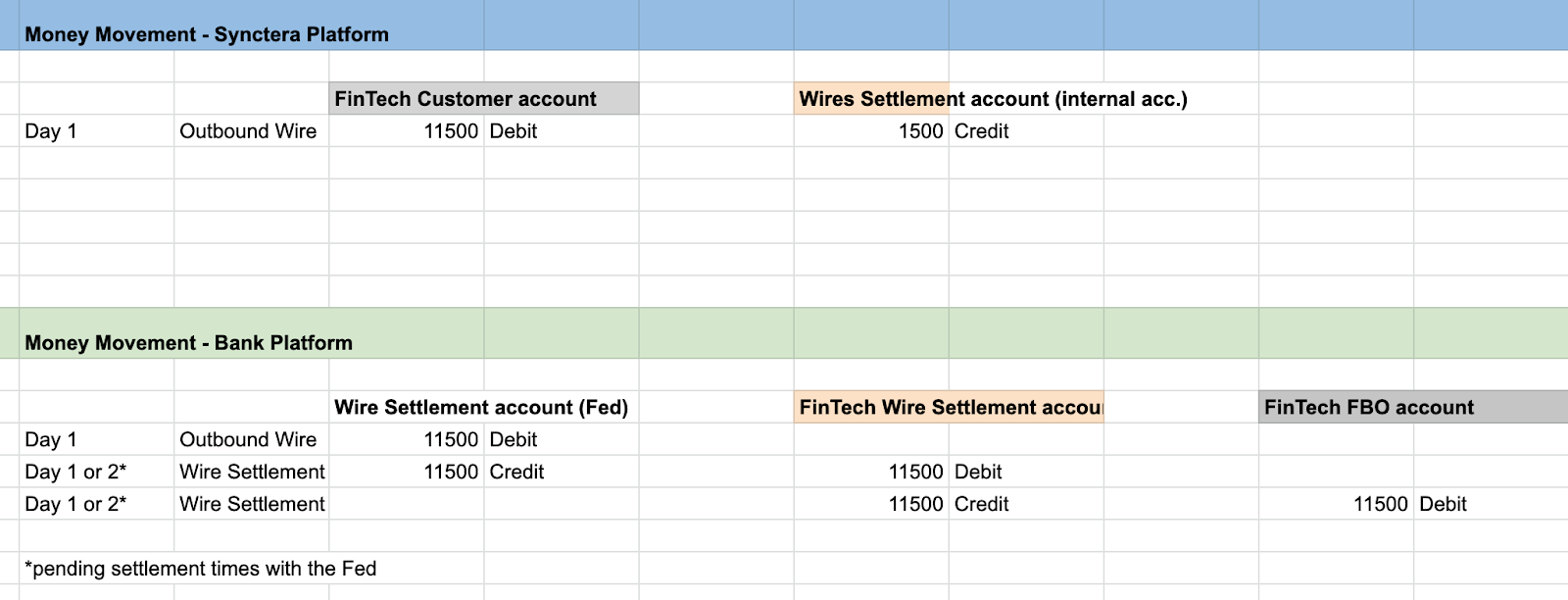

Outbound file processing (From FinTech to Bank and to Fed)

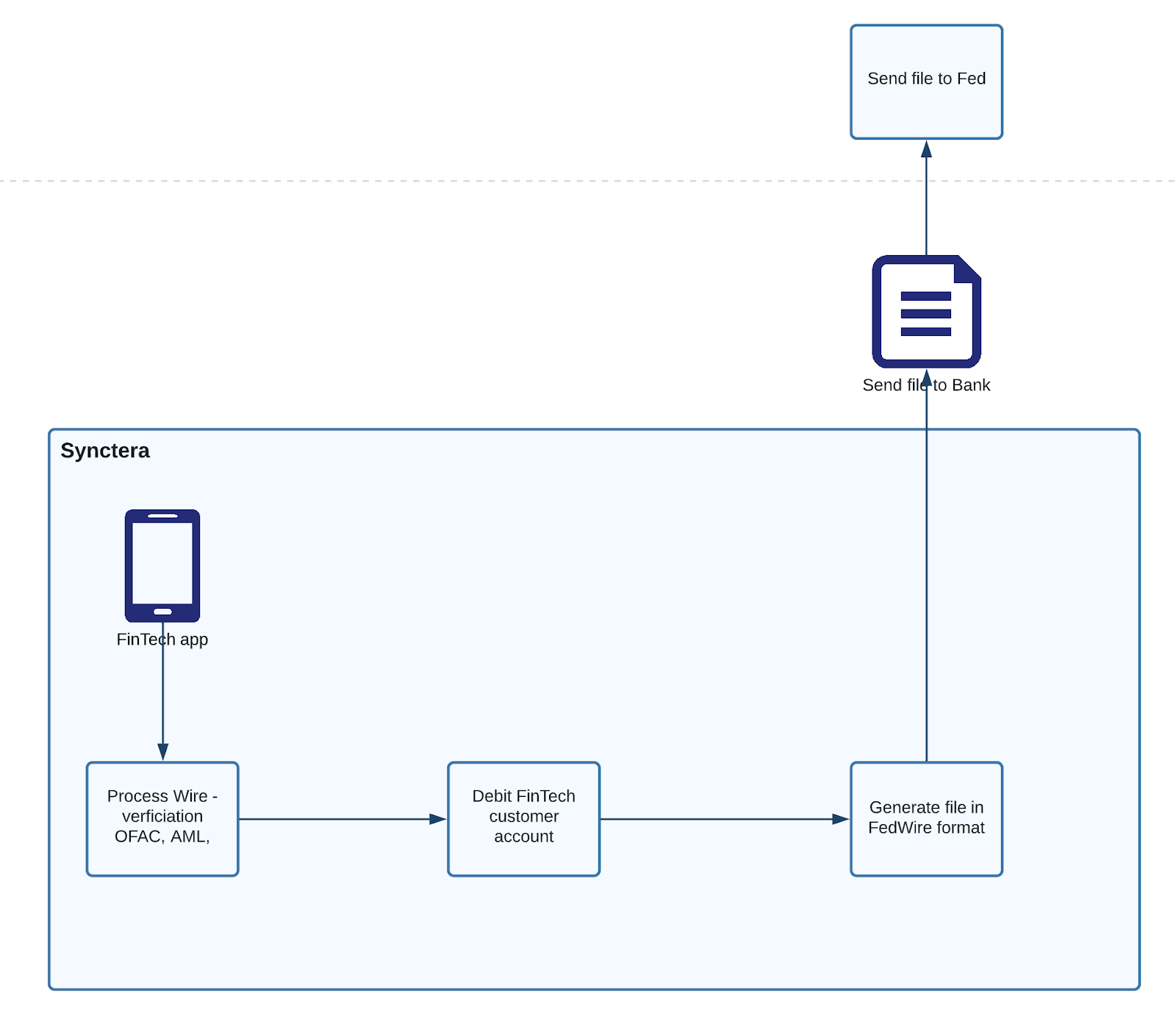

FinTechs at Synctera can create Wire transfers debiting their customer accounts. The standard validation checks are performed when the FinTech creates the Wire transfer (balance check, OFAC, AML, fraud, limits, ect). Most banks have the capability to receive Wire files in FedWire format and exchange it to the Fed, a common capability used to serve business customers. The process works as follows:- Synctera FinTech users create a Wire transfer sending money to an external bank. The data that is needed to generate a Wire transfer is:

- Recipient name (Company name or person name)

- Recipient address (Company/Person address)

- Amount

- Recipient account number

- Recipient bank name (optional)

- Syntera runs transaction checks for the transaction (limits, account balance, OFAC, AML…)

- FinTech customer account is debited, Wire transaction ID is generated

- File is created with Wire entry in FedWire format. Synctera holds wire files for 30 minutes in case of end-customer driven cancellations.

- File is sent to bank via SFTP

- Bank sends file to Fed for exchange

- Posting entries for the wire will be generated same day, and sent via the normal autosweeps file

International Wires exchange with Synctera

Some FinTechs are interested in receiving and sending international wires. Initially we expect low volumes on International Wires.Inbound file processing (From SWIFT / Third Party provider to Sponsor Bank)

To process inbound Wire files, we will follow a similar approach above. The following needs to be considered:- The transaction will be posted to the Wires Settlement account in the bank core system in USD

- The bank will provide Synctera with the currency exchange rate applied to the transaction

Flow of funds

Inbound Wires (From Fed to Bank)

Outbound Wires (From Bank to Fed)