Overview

For transactions on FinTech-issued cards, end-users can initiate disputes through the Synctera platform. For Instant Account Funding / AFT and Instant Push-To-Card / OCT transactions, on the other hand, the FinTech acts as the merchant, accepting transactions on cards that are issued by other financial institutions. Those externally-issued card transactions must be disputed through the issuing financial institution, which submits it to the network. The network then notifies the acquiring financial institution, i.e. the bank that enables the merchant to accept payments, about the dispute, and the dispute progresses through the dispute lifecycle. As the acquiring processor, TabaPay, ensures that Synctera is notified about the dispute and its progress, and Synctera manages the dispute on the FinTech’s/merchant’s behalf. The External Card Dispute case is used for tracking disputes of AFTs/OCTs. In fact, disputes of OCTs are extremely rare, and almost all external card transaction disputes occur on AFTs. The dispute flow and the case management process is described in the sections below.Best practices

For best practices on how to prevent disputes and chargebacks on AFTs/OCTs, see this section.External Card Dispute investigation / lifecycle

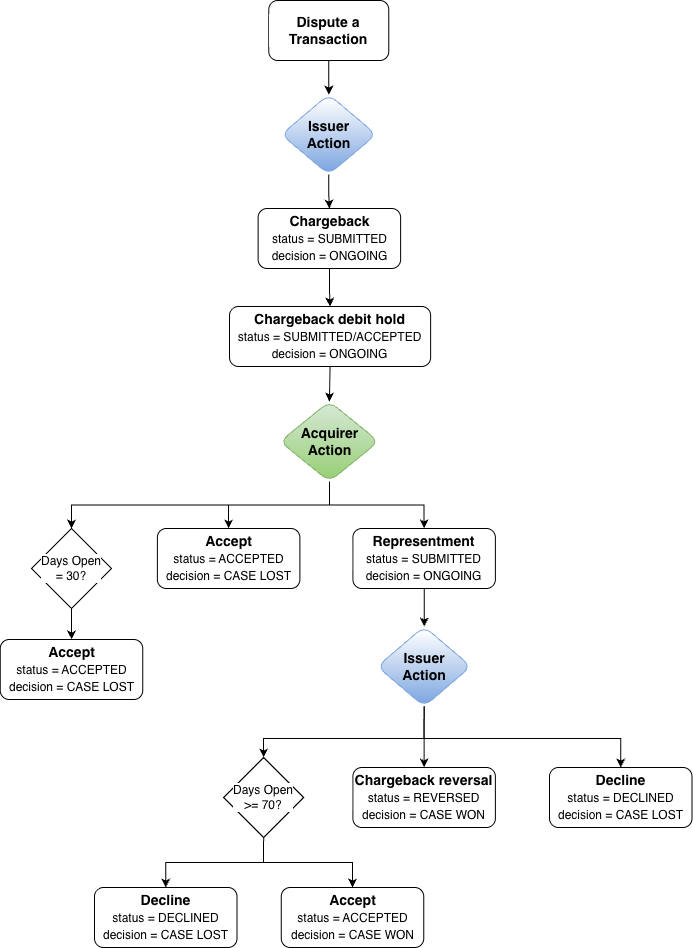

The management lifecycle of an AFT/OCT dispute is shown below. Any updates are notified through email and webhooks.

- Dispute/chargeback submitted with issuer: Cardholder submits a dispute to the card issuer (external), who submits a chargeback to the network.

- Acquirer/merchant is notified of chargeback: The acquiring processor, TabaPay, notifies Synctera about the chargeback. This triggers an automatic creation of an External Card Dispute and case in the Synctera Console.

- Case status:

New -> Action required - Dispute status:

Chargeback: SubmittedandDecision: Ongoing - FinTech’s AFT/OCT Chargeback DDA is debited for the dispute amount through incoming ACH

- Case status:

- Provisional debit hold is placed on customer’s account: To prevent further loss, a provisional chargeback debit hold is automatically placed on the customer’s account while the dispute is under investigation.

- Case status:

Action required - Dispute status:

Chargeback: SubmittedandDecision: Ongoing - Debit status:

Provisional(Chargeback Debit Submitted)

- Case status:

- Acquirer/merchant action - response deadline: The FinTech has 10 calendar days from the chargeback submission (exception) date to file a representment with their evidence.

- No action or late submission will automatically result in case being lost and closed:

- Case status:

Decision -> Closed - Dispute status:

Chargeback: AcceptedandDecision: Lost - Debit status:

Final(Chargeback Debit posted)

- Case status:

- No action or late submission will automatically result in case being lost and closed:

- Representment is filed by merchant: This is the only actionable step on the FinTech’s side (all other dispute transitions are automated). Through the Synctera Console, FinTech files a representment with their evidence. Synctera reviews the evidence for completeness and compliance before forwarding it to TabaPay, which represents the transaction to the network.

- Case status:

In review - Dispute status:

Representment: SubmittedandDecision: Ongoing

- Case status:

- Issuer response, network review & resolution: There are several different outcomes based on the issuer’s response and the network’s review of the FinTech’s documentation and the issuer’s claim.

- Recall case - merchant wins:

- Case status:

Decision -> Closed - Dispute status:

Chargeback: ReversedandDecision: Won - Debit status:

None(Provisional Chargeback Debit hold is deleted) - FinTech’s AFT/OCT Chargeback DDA is credited for the dispute amount through incoming ACH

- Case status:

- Accept representment - merchant wins:

- Case status:

Decision -> Closed - Dispute status:

Representment: AcceptedandDecision: Won - Debit status:

None(Provisional Chargeback Debit hold is deleted) - FinTech’s AFT/OCT Chargeback DDA is credited for the dispute amount through incoming ACH

- Case status:

- Decline representment/evidence - merchant loses:

- Case status:

Decision -> Closed - Dispute status:

Representment: DeclinedandDecision: Lost - Debit status:

Final(Chargeback Debit posted)

- Case status:

- Recall case - merchant wins:

What’s displayed for External Card Dispute cases

Case status

The case status is shown at the top of the Dispute case - to the right of the case description.

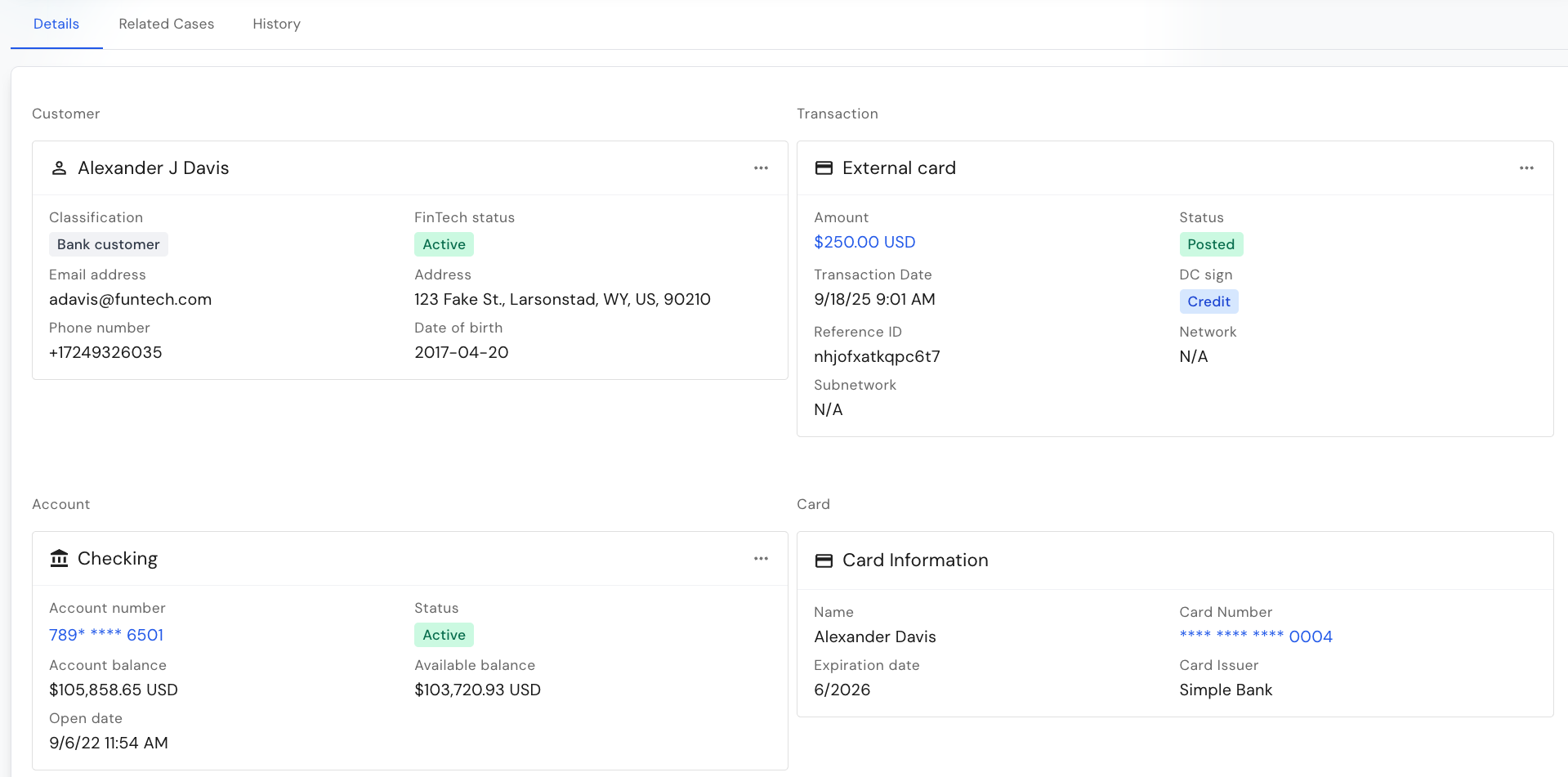

Customer, account, card, transaction

The first section in the Details tab shows the Customer, Account, External Card, and AFT/OCT Transaction to which the dispute belongs. To view more details on each object, follow the link under the relevant object.

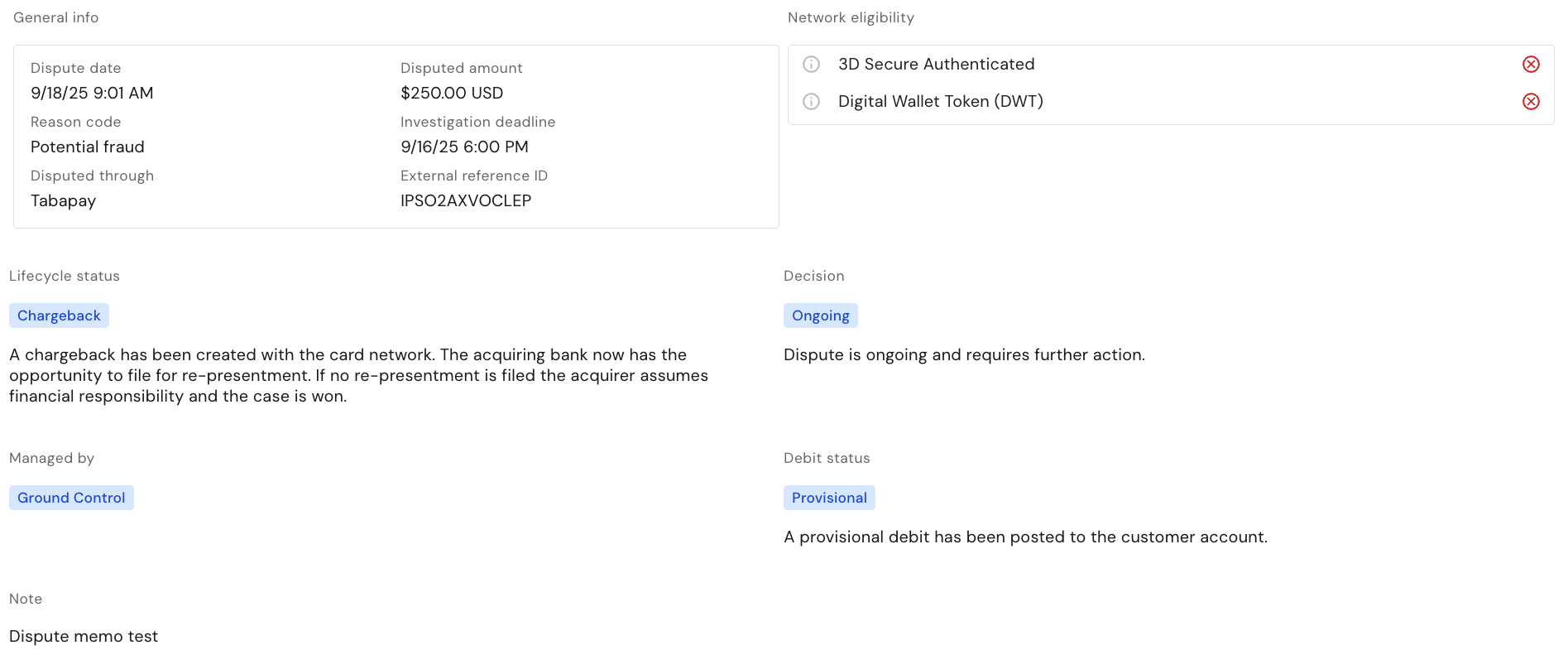

General info and lifecycle status

The second section in the Details tab shows general information about the dispute as well as the dispute status (see dispute investigation/lifecycle flow diagram above):- Lifecycle status:

Chargeback / Representment - Decision:

Ongoing / Won / Lost - Debit status:

Provisional / Final / None - Managed by:

Ground Control(all External Card Dispute cases are managed by GC)

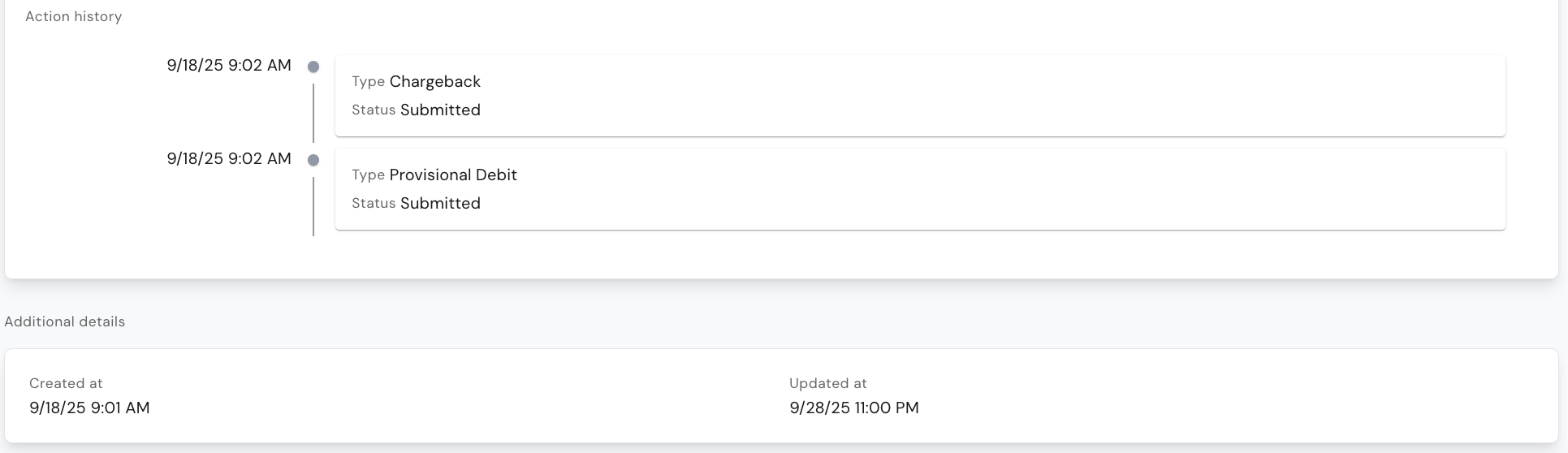

Action history

The second section in the Details tab shows the dispute action history along with creation and last modification date:

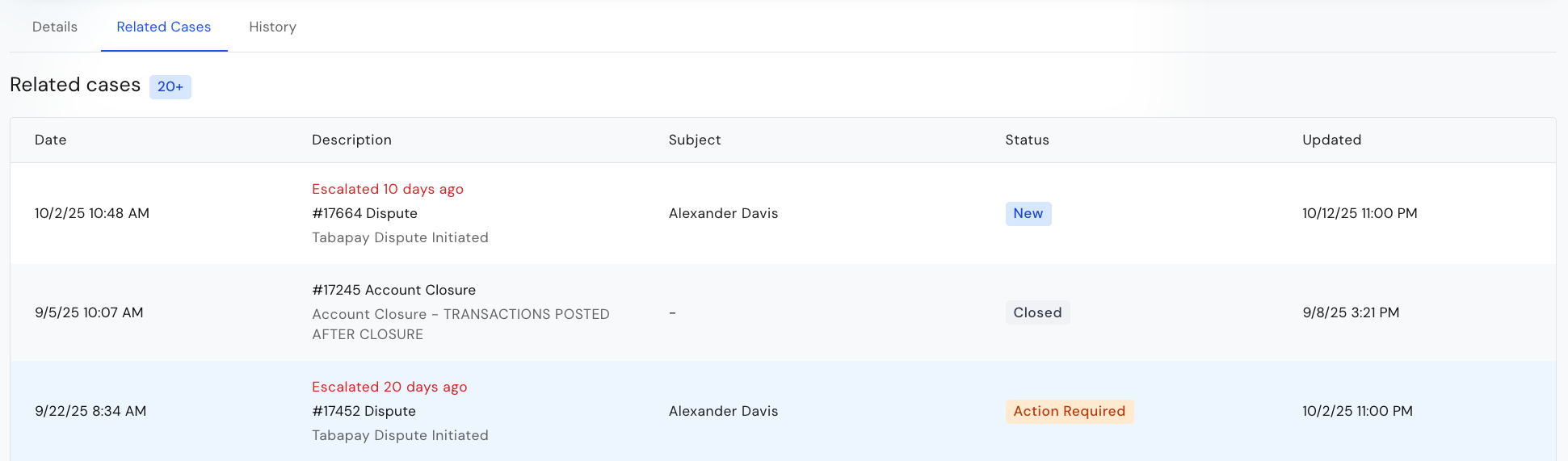

Related cases

The second tab on the case shows all other cases for the same customer:

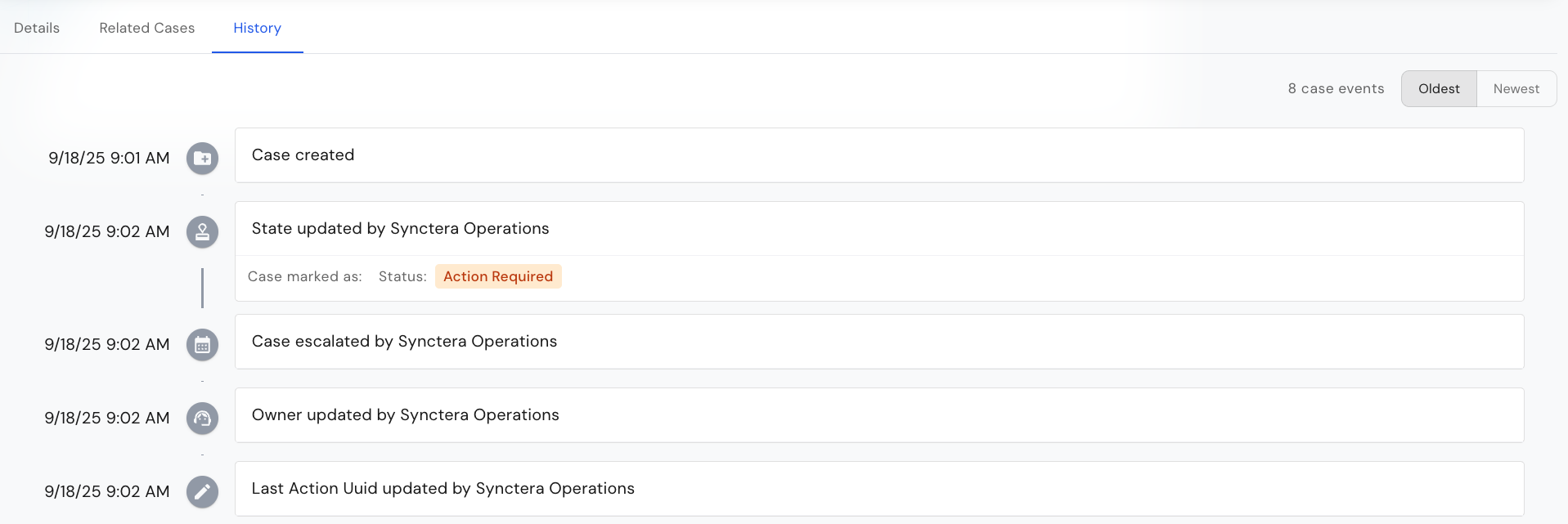

History

The third tab on the case shows the case history, i.e. all the case status transition:

How to action External Card Dispute cases

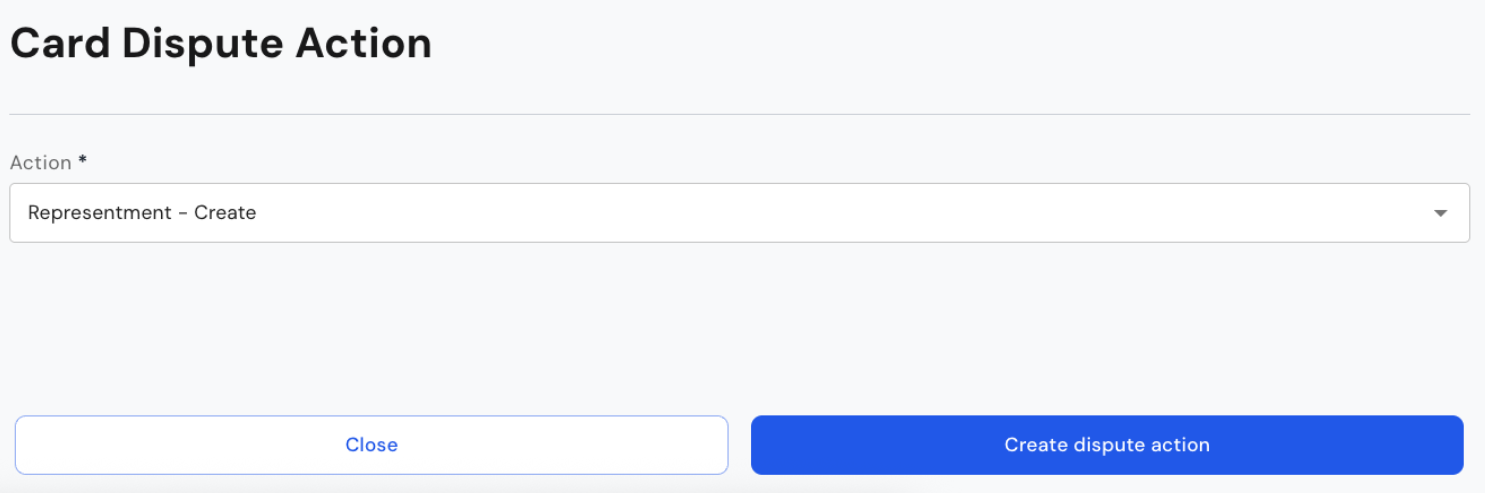

Representment

To file a representment, go to Actions -> Take Dispute Action and select Representment - Create from the dropdown:

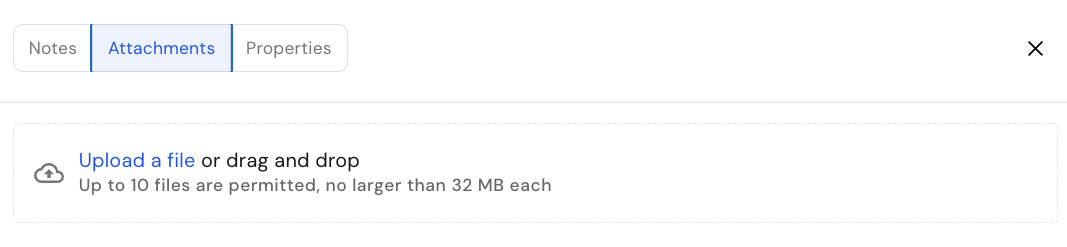

Upload evidence

To upload evidence, go to Attachments -> Upload a file. For submission standards, see this section.

How to monitor External Card Dispute cases

Emails and webhooks

Any time the dispute case status changes or a note is added, an email is automatically sent to case assignees. Another way to get notified about the status of the case/dispute is to subscribe toDISPUTE webhooks, which are triggered anytime a dispute is created or updated.